Services

Payroll, benefits, HR, and risk management in one PEO model built to lighten the load for small businesses.

Finding the best workers comp insurance for a small business isn’t about picking one specific provider. It’s about choosing the right model for your company’s size, risk level, and how much administrative work you can handle internally. For many growing businesses, a Professional Employer Organization (PEO) is a smart move, bundling coverage with expert risk management and payroll. But direct insurers and state funds still have their place, depending on your situation.

Choosing workers’ compensation insurance is a massive decision for any small business owner. This isn’t just another line item in your budget; it’s a legal requirement in nearly every state and the primary safety net for your employees. Getting a handle on your options is the first step toward a choice that protects both your team and your bottom line.

This guide is here to demystify the process and help you sort through the different ways you can get coverage. For business leaders, particularly those managing teams of 20 to 150 employees, this roadmap will help you think beyond just checking a compliance box and make a strategic decision that actually supports your company’s growth.

At its heart, workers’ compensation is a no-fault insurance system. It covers medical bills and lost wages for employees injured on the job. In return, employees generally give up their right to sue their employer for negligence related to the workplace injury.

As a small business, you usually have three main ways to get this coverage. Each one comes with a different mix of cost, administrative effort, and hands-on risk management support. Weighing these trade-offs is how you’ll find the right fit.

| Coverage Model | Core Benefit | Primary Consideration |

|---|---|---|

| Direct Insurer | Potentially lower premiums if you’re in a low-risk industry. | Demands significant in-house administrative work. |

| State Fund | Often the go-to insurer for high-risk businesses. | Service and support levels can be wildly inconsistent. |

| PEO Partnership | Integrated risk management, claims support, and payroll. | Best fit for businesses wanting to outsource HR administration. |

In the end, the goal is to land on a solution that does more than just keep you legal. The right partner will help you build a safer workplace, get a grip on long-term costs, and take the administrative load off your plate so you can focus on running your business.

To find the right workers’ comp insurance for your small business, you have to look past the sticker price of the premium. The final cost you pay is a mix of several interconnected factors, each one shaped by your industry, your safety record, and even your administrative accuracy. Getting a handle on these moving parts is the first real step toward reining in your costs.

The premium calculation starts with a fairly standard formula, but the details inside it are what really matter. At its heart, the math involves your total payroll, the risk tied to the kind of work your employees do, and your company’s unique claims history. Nailing this is critical for smart budgeting and avoiding nasty financial surprises down the road.

The starting point for your premium is your gross payroll. Insurers begin here because it’s a clear measure of exposure—more employees and higher wages mean more potential for claims. For every $100 of payroll, the insurance carrier applies a specific rate.

But not all payroll is created equal. This is where employee classification codes, or “class codes,” come into the picture. These four-digit codes, managed by bodies like the National Council on Compensation Insurance (NCCI) or independent state rating bureaus, sort employees into categories based on their job duties and the risks that come with them.

A roofer, who is in a high-risk job, will have a much steeper rate applied to their portion of the payroll than a clerical worker at the same company. If you misclassify an employee, even by accident, you could be looking at significant penalties and a large bill for back premiums when it’s time for an audit.

Your Experience Modification Rate (EMR)—sometimes called an Experience Mod or X-Mod—is a huge multiplier in your premium calculation. Think of it as a direct reflection of your company’s claims history when compared to other businesses in your field.

The industry average EMR is 1.0.

A strong safety culture doesn’t just prevent injuries; it directly cuts your insurance costs. A low EMR is concrete proof that your risk management efforts are working, making you a more attractive client to insurers and saving you real money.

If you’re a new business without a claims history to analyze, your EMR will usually start at the industry average of 1.0. Over time, typically after three years of claims data is available, your own unique EMR is calculated. This creates a powerful incentive to keep your workplace safe.

Workers’ compensation policies are built on estimated payroll for the year ahead. But payroll is rarely static—it changes with new hires, raises, and overtime. Because of this, insurers conduct a payroll audit at the end of your policy term to square the estimate with what you actually paid out.

If your real payroll was higher than you projected, you’ll get a bill for the extra premium you owe. On the flip side, if it was lower, you might be due a refund. This process is standard, but it can create unexpected cash flow headaches for businesses that aren’t tracking their payroll carefully all year. For a deeper dive, you can learn more about calculating workers’ comp premiums and how to save.

Beyond the premium, the true cost includes the hidden fallout from a claim. You have lost productivity from an injured employee, the administrative hours spent managing the claim, and the potential hit to team morale—all very real costs. These factors, combined with the long-term impact on your EMR, make proactive safety and claims management a financial necessity, not just a nice-to-have.

Choosing how to handle workers’ compensation is a bigger decision than most small business owners realize. It’s not just about checking a legal box. It’s about finding a coverage model that fits your company’s risk, your team’s administrative capacity, and your plans for growth. The best workers’ comp insurance for your business is the one that strikes the right balance between cost, effort, and expert support.

Let’s move past the simple pros and cons and dig into the three main ways you can get coverage: buying directly from an insurer, using a state-sponsored fund, or partnering with a Professional Employer Organization (PEO). We’ll look at each one based on what actually matters to a growing business.

Going straight to a private insurance carrier is the traditional route. You work with an agent or broker to get a policy from a commercial provider. For the right kind of business, this can be a perfectly straightforward and affordable solution.

This option is usually a good fit for businesses in low-risk industries—think professional services or consulting—that have a great safety record and a low Experience Modification Rate (EMR). It also assumes you have someone on your team, like an HR manager or a sharp office manager, who can handle all the administrative work that comes with managing a policy.

Some states run their own workers’ compensation insurance funds. These state-operated entities often act as an insurer of last resort, making sure even high-risk businesses can get the coverage they’re legally required to have.

A new construction company or a small manufacturing firm that’s been turned down by private insurers might find a state fund is their only option. It’s also important to know that in four states—North Dakota, Ohio, Washington, and Wyoming—the state fund is monopolistic, meaning businesses generally must buy their coverage from the state.

State funds serve a critical purpose by ensuring universal access to coverage. But the trade-off for that accessibility can sometimes be less personal service and fewer integrated risk management tools than you’d find with private options.

Service quality and pricing can be inconsistent from one state to the next. While some funds are competitive, others might have higher rates and offer minimal support, feeling more like a government agency than a strategic partner.

A Professional Employer Organization (PEO) provides an entirely different model. Through what’s called a co-employment relationship, your business gets access to the PEO’s master workers’ compensation policy. This isn’t just an insurance plan; it’s a complete, managed risk and safety solution.

This approach is ideal for small to midsize businesses (think 20-150 employees) looking to offload administrative headaches, get access to more competitive rates, and have experts guide them on safety and claims. It’s especially powerful for companies expanding into new states or those in industries where actively managing risk can make a huge difference to the bottom line.

To make the decision clearer, it helps to see the options laid out side-by-side. Each model has its place, and the best fit depends entirely on your business’s specific circumstances.

| Coverage Option | Best For | Cost Structure | Administrative Burden | Claims & Risk Support |

|---|---|---|---|---|

| Direct Insurer | Low-risk businesses with a strong safety record and in-house administrative capacity. | Up to 25% down payment plus installments; premiums tied to EMR and annual payroll audit. | High: Your team handles all claims filing, paperwork, and audit preparation. | Varies: Often generic resources; you manage claims processes internally. |

| State Fund | High-risk businesses, startups, or those unable to secure private coverage. Mandatory in 4 states. | Premiums based on state-set rates; structure varies. | Moderate to High: Can be bureaucratic and require significant follow-up. | Minimal: Primarily focused on processing claims, not proactive risk management. |

| PEO Partnership | Small to midsize businesses (20-150 employees) seeking to reduce admin, improve safety, and manage cash flow. | No large down payment; premiums paid per payroll cycle. | Low: PEO manages claims, safety programs, and the annual audit. | Comprehensive: Dedicated experts provide safety training, claims management, and support. |

Ultimately, this table highlights the core trade-offs: cost predictability, administrative workload, and the level of expert support you receive when an incident occurs.

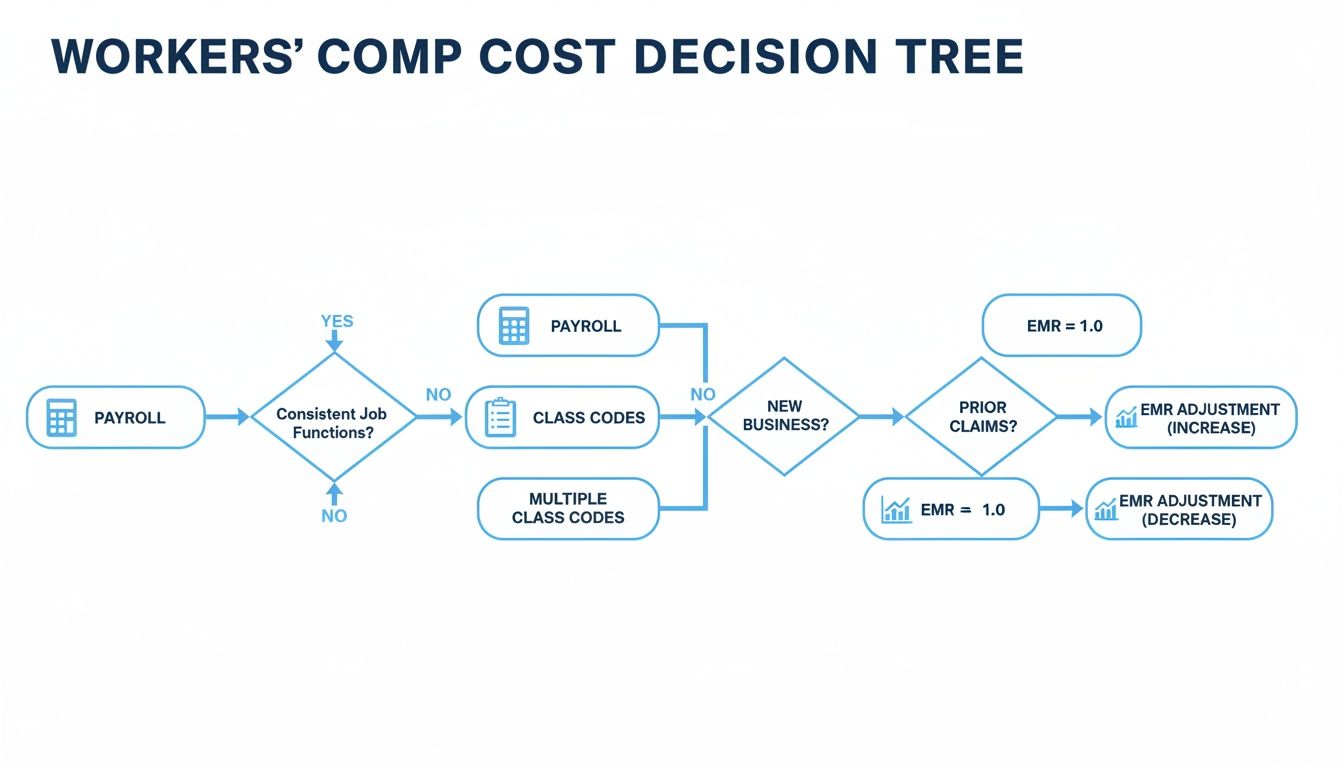

The decision tree below helps visualize how factors like payroll, class codes, and EMR directly impact your workers’ compensation costs, which in turn can help point you toward the right coverage model.

This visual shows how a single workplace injury can create a ripple effect, driving up your EMR and premiums for years. It’s a risk that the integrated support from a PEO is designed to help control.

The workers’ compensation market has been shaped by long-term declines in claim frequency, while medical and indemnity costs remain an ongoing concern for employers. NCCI’s most recent State of the Line reporting highlights that frequency has continued to trend downward over time, even as claim costs and other market pressures remain key considerations. For small businesses, that means pricing can stay competitive, but a single serious claim can still have a lasting impact on premiums through experience rating.

Workers’ compensation isn’t a federal program; it’s managed entirely at the state level. That means the rules can change dramatically the moment your business crosses a state line, creating a complex web of regulations that can easily trip up a growing company. (Note: Texas is the only state where workers’ comp is optional for most private employers).

One of the biggest differences you’ll see is the employee threshold for mandatory coverage. In most states, you’re required to get a policy as soon as you hire your first employee. But there are exceptions. South Carolina, for example, generally requires it only for businesses with four or more employees, while several other states have a threshold of three or five.

Beyond just how many employees you have, states also differ on who counts as an employee. The rules for classifying workers as W-2 employees versus 1099 independent contractors are notoriously tricky and vary widely. Misclassifying someone can lead to serious penalties, including back taxes, fines, and liability for past injuries.

Some states also have unique systems that limit your insurance options. These are known as monopolistic states.

A common mistake we see is when a growing business assumes the rules from their home state apply everywhere. A company based in Arizona that hires a remote worker in Wyoming will find itself out of compliance fast if it doesn’t get coverage through Wyoming’s state fund.

As businesses grow and hire remote employees, keeping up with these distinct state requirements becomes a huge administrative burden. Each new state means a new set of rules for payroll reporting, claims processing, and required workplace safety postings. For a small business, staying on top of it all is critical. And while we’re focused on the U.S., looking at frameworks like the Australian workplace safety standards shows just how important meticulous compliance is globally.

This is where partnering with an expert becomes invaluable. A PEO that specializes in multi-state compliance already has the infrastructure and knowledge to handle these headaches. Instead of you having to research and get policies in each new state, a PEO handles the registration, ensures you’re following local laws, and manages all the state-specific reporting under one roof. Our multi-state employment compliance guide dives deeper into these challenges.

That kind of expert oversight is crucial for minimizing legal risks and letting you focus on growth without constantly worrying about state-by-state compliance hurdles.

To find the right workers’ comp insurance, you have to look past the policy features and dig into the real-world risks that are actually driving your costs. Sure, premiums start with payroll and class codes, but certain dynamics in your workplace can quietly send your claims—and your costs—through the roof.

Figuring out these risk factors is the first step toward building a safety strategy that works. Things like employee experience, the age of your workforce, and even shifting attitudes about workplace health are creating new challenges. If you ignore them, you’re leaving your business exposed to claims that could have been avoided.

One of the biggest drivers of risk is simply inexperience. New hires are still learning the ropes, especially in roles that involve physical labor or specialized equipment. It’s no surprise they’re more likely to have an accident. This is a huge deal for businesses that are growing fast or dealing with high turnover.

This trend is particularly relevant right now. The workers’ comp market is still pretty good for small businesses, but NCCI data shows that newer, less experienced workers are twice as likely to get injured on the job. For small business owners in professional fields in cities like Nashville, Denver, or Dallas, this signals a growing risk even in what we think of as “safe” office settings.

If you really want to get a handle on how premiums are set, understanding workers’ compensation class codes is non-negotiable. They’re the foundation for classifying your business’s risk level.

On the other end of the spectrum, an aging workforce brings a different set of challenges. While veteran employees know your safety protocols inside and out, they also face a higher risk of getting more seriously hurt from things like slips, trips, and falls.

As more people work past the traditional retirement age, we’re seeing a rise in claims for injuries like fractures and muscle tears. These almost always mean longer recovery times and much higher medical bills. Projections show that by 2032, workers over the age of 55 will account for 25% of all claims—a stat that should make every business owner think about ergonomic assessments and safety programs designed for an older demographic.

A single severe injury can have a long-lasting financial impact, driving up your Experience Modification Rate (EMR) for years. By focusing on preventative measures for all age groups, you protect both your employees and your company’s financial health.

These two trends—a flood of new workers and a growing number of older ones—make a powerful case for getting strategic about risk. Turning a blind eye to these realities just leaves you vulnerable to predictable, expensive claims that a solid safety culture and the right expert guidance could have helped you avoid.

After weighing your options, you might realize that just buying an insurance policy isn’t going to cut it. For many growing small businesses, the best workers’ comp solution is one that comes with a built-in team of experts. This is exactly where partnering with a Professional Employer Organization (PEO) becomes a strategic move.

A PEO is often the right fit for small to midsize businesses, typically those with 20 to 150 employees, that are starting to feel the pressure of administrative overload. If you’re fighting rising insurance premiums, struggling with claims management, or hiring employees across state lines, a PEO provides a powerful, all-in-one solution.

The PEO model is built on a concept called co-employment. Through this arrangement, your business gets access to the PEO’s master workers’ compensation policy. This immediately unlocks two huge benefits: more competitive rates and greater premium stability, since your company’s risk is pooled with hundreds of other businesses.

More importantly, a PEO delivers comprehensive risk management services, not just an insurance plan. This is a critical distinction. Instead of leaving you to handle claims and safety on your own, the PEO becomes an active partner in protecting your business and your people.

This partnership includes a full suite of services designed to control your long-term costs:

The hands-on support from a PEO directly impacts your bottom line by reducing both how often claims happen and how severe they are. Severe injuries can drive claim costs quickly. For example, the National Safety Council reports that lost-time workers’ compensation claims involving amputation averaged about $125,058 (2022–2023 claims), while fracture, crush, or dislocation averaged about $66,467. These figures show why prevention, fast reporting, and a strong return-to-work process matter for long-term cost control.

These figures show why small businesses in hands-on industries often face steep premiums with no clear strategy to lower them. For growing companies, especially those in business services across states like Utah, Idaho, Arizona, and Wyoming, these numbers highlight an urgent need for support. You can explore more data on workers’ compensation claim costs to see the full picture.

For many business owners, the true value of a PEO is peace of mind. Knowing that a team of experts is managing compliance, claims, and safety allows you to stop worrying about HR administration and focus entirely on growing your company.

By offloading these complex responsibilities, you free up valuable time and internal resources. A PEO partnership provides the structure and expertise needed to create a safer work environment, control your insurance costs, and support your employees when they need it most.

Our guide explains in detail how a PEO can reduce risk for small businesses and protect your long-term financial health. This shift from a reactive to a proactive approach is often the key to sustainable growth.

Navigating workers’ compensation can bring up a lot of questions about compliance, coverage, and strategy. We work with small business owners on these issues all the time, and a few questions pop up more than others.

Here are clear, straightforward answers to the most common ones we hear.

Operating without legally required workers’ comp coverage is a huge gamble. State penalties are severe and can include steep daily fines, stop-work orders that shut down your business, and even criminal charges.

But the financial risk goes even deeper. Without a policy, you lose your protection from civil lawsuits. If an employee gets injured on the job, you could be held personally liable for their medical bills and lost wages—a financial hit that many small businesses simply can’t recover from. In states where coverage is optional, like Texas, choosing not to carry a policy still leaves your business open to negligence lawsuits from injured employees.

This is one of the most common questions we get, and the answer depends entirely on your state’s laws and your business structure. In many states, sole proprietors, partners, and certain LLC members or corporate officers can legally opt out of carrying coverage for themselves.

In other states, however, everyone who performs work for the company, including owners, must be covered. It’s absolutely critical to check your specific state regulations because making the wrong assumption here can leave you non-compliant and exposed to unexpected liability.

Always verify owner exemption rules with your state’s workers’ compensation board or an expert partner. An incorrect assumption here can create a costly gap in your company’s legal and financial protection.

This is where a PEO really shines. A PEO simplifies multi-state operations by managing all the different state-specific requirements under its own master insurance policy. When you hire an employee in a new state, you don’t have to go out and shop for a new policy or get up to speed on a whole new set of rules.

The PEO handles all the necessary state registrations, ensures the policy meets local laws, and manages the payroll reporting for premiums. This centralized approach is especially valuable for navigating the complexities of monopolistic states, significantly cutting down your administrative burden and compliance risk.

Finding the best workers’ comp insurance for your small business means choosing a partner who can manage risk, simplify compliance, and protect your team. Helpside provides an integrated solution that combines competitive coverage with expert risk management, freeing you to focus on growth. Learn how Helpside can support your business at https://www.helpside.com/benefits-audit/.