Services

Payroll, benefits, HR, and risk management in one PEO solution.

A renewal meeting should not feel like a survival exercise. Yet for many small business owners, it does.

You review your general liability, commercial auto, and workers’ compensation program. Everything looks normal until someone asks a simple question: what happens if one claim blows past your base limits? That is the moment many owners realize they are insured for common losses, but not necessarily protected from a severe one.

Commercial umbrella insurance sits in that gap. It is not a luxury product for giant companies. It is a practical layer of asset protection for businesses that have employees, clients, contracts, vehicles, visitors, or any significant chance of causing a serious third-party loss.

A business can do almost everything right and still end up in a lawsuit that changes the year.

An employee drives to a client meeting and causes a serious crash. A visitor falls in your office and suffers a long-term injury. A claim starts as a routine incident, then legal costs rise, damages rise, and your underlying policy limit suddenly looks small. Once that primary limit is exhausted, the unpaid portion does not disappear. It lands on the business.

That is the practical reason commercial umbrella insurance matters. It provides an additional layer of liability protection above certain underlying policies when a covered loss grows beyond those base limits.

This need is not theoretical. The global commercial umbrella insurance market is projected to reach $18.12 billion in 2025, growing at 10.1%, driven in part by the rising frequency of “nuclear verdicts”, meaning jury awards above $10 million, according to Stats Market Research’s commercial umbrella insurance forecast.

Many owners buy liability insurance assuming the policy they already have is enough for the worst day they can imagine.

That assumption breaks down when a loss involves severe bodily injury, multiple claimants, or a lawsuit that keeps expanding. The policy may still work exactly as written. The problem is that the limit may not be high enough.

Commercial umbrella insurance is often the policy that keeps one bad event from turning into a balance-sheet problem.

It can also protect growth. A major uncovered liability claim does more than create legal expense. It can disrupt hiring, delay expansion, strain cash flow, and force ownership to make decisions from a defensive position.

Practical takeaway: Umbrella coverage is not about expecting disaster. It is about acknowledging that severe claims happen faster than most owners expect, and standard liability limits are often built for ordinary losses, not catastrophic ones.

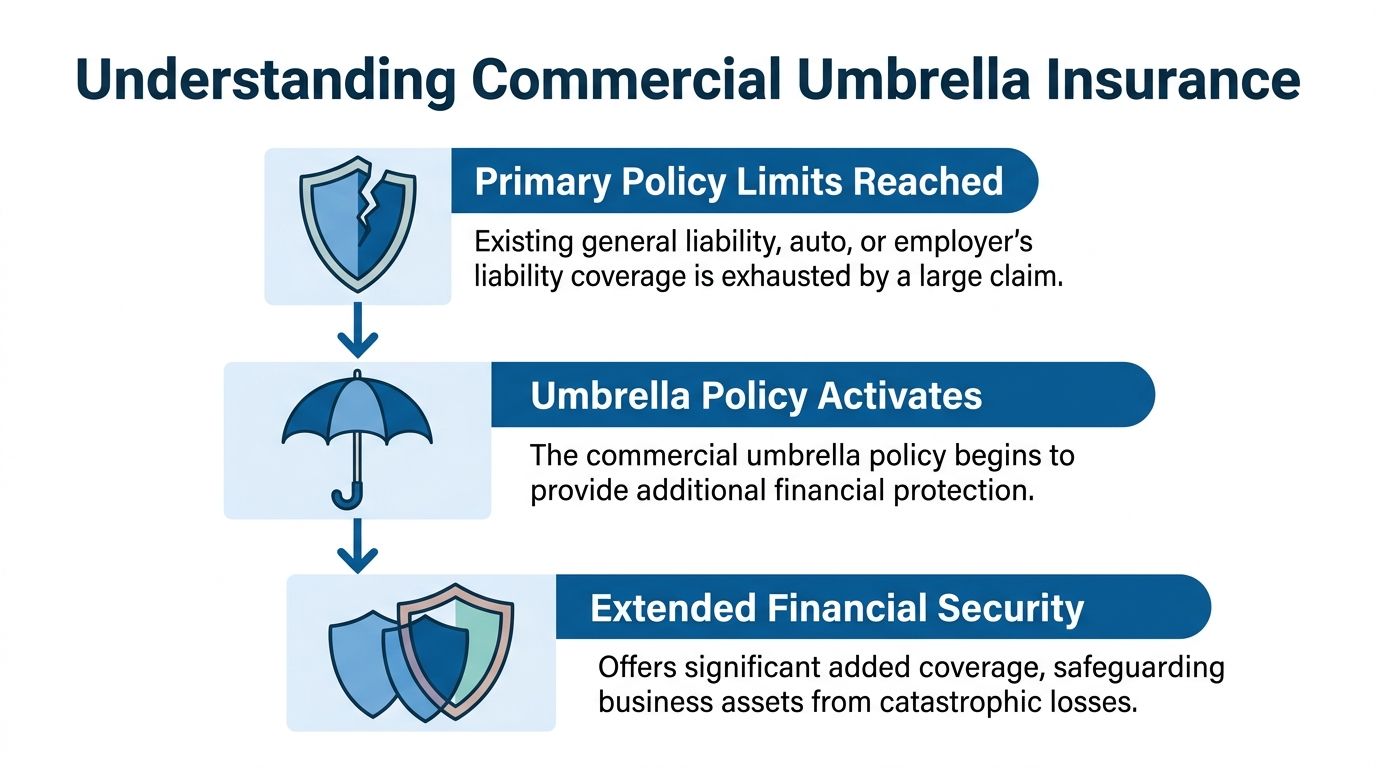

Think of your liability program as a stack, not a single policy.

At the bottom are your underlying policies, typically general liability, commercial auto liability, and employer’s liability. Commercial umbrella insurance sits above them. It does not usually pay first. It responds after a covered underlying policy has paid up to its limit.

If a covered claim hits your general liability policy first, that policy pays until its limit is exhausted. Then the umbrella policy can begin paying covered amounts above that threshold.

The same structure can apply over other scheduled underlying policies, depending on how your insurance program is built.

A simple way to picture it:

| Layer | What it does |

|---|---|

| Primary policy | Handles the claim first, up to its stated limit |

| Commercial umbrella insurance | Adds another layer of protection after the primary limit is exhausted |

| Business assets | Remain exposed if the claim exceeds both layers or falls outside coverage |

Many buyers assume umbrella insurance means “extra coverage for anything liability-related.” That is not how it works.

Coverage is tied to the underlying program and to the umbrella form itself. A covered underlying claim can move up into the umbrella layer after the base limit is exhausted. But a claim that is excluded, or not properly structured in the underlying program, may not be picked up the way the buyer expects.

There is another important mechanic that gets overlooked during quoting. Self-insured retention, often called SIR.

Commercial umbrella coverage only triggers after underlying primary policy limits are exhausted. For claims covered by the umbrella but not the primary policy, a Self-Insured Retention, often starting at $10,000, must be paid by the insured before the umbrella policy responds, according to Insureon’s explanation of how umbrella insurance works.

That matters because SIR is not the same as the deductible business owners are used to seeing on other policies.

A deductible usually applies within the primary policy structure. SIR is different. It is the amount the insured must absorb before the umbrella responds in a situation where the umbrella provides coverage that the underlying policy does not.

That creates a practical budgeting issue.

The term “umbrella” is useful because one policy can extend above several underlying liability lines at once. Instead of trying to raise each underlying line independently, the umbrella creates one higher layer over the scheduled foundation.

That is why the policy can be efficient when structured well.

It is also why mistakes in the foundation matter so much. If the underlying program is weak, misaligned, or incomplete, the umbrella does not fix that by itself.

Tip: Ask for a plain-language explanation of exactly which underlying policies your umbrella sits over, where the attachment points are, and when any SIR applies. If the answer is vague, keep asking.

A lot of owners still assume commercial umbrella insurance is mainly for construction firms, trucking companies, or manufacturers.

Those businesses certainly need to think about it. But many white-collar companies need it too, often for a completely different reason. Their exposure is not always physical hazard. It is contractual pressure, employee activity, and the growing seriousness of third-party claims.

For low-risk, white-collar businesses such as consultants or attorneys with 10 to 75 employees, the need for umbrella insurance is often driven by contractual requirements from larger clients demanding $5M+ in liability coverage. That contractual exposure is a primary driver of the estimated 75% underinsurance rate among small businesses, according to Christensen Group’s guide to commercial umbrella insurance.

That is why a business can look “low risk” on paper and still need higher liability limits.

An enterprise client may require elevated limits before signing a services agreement. A landlord may require broader protection in a lease. A customer procurement team may treat higher limits as a baseline condition, not a negotiated item.

A business does not need heavy equipment or a warehouse full of inventory to face liability severity.

Here are the triggers that come up often for small and midsize service firms:

Professional services firms are a common example. So are agencies, SaaS companies, consulting firms, and business services companies.

Their leadership teams often focus on professional liability, cyber, and employment practices. Those are important. But they can miss bodily injury, auto, and employer’s liability exposures because those feel less central to the business model.

That is a mistake.

A white-collar company may not be high hazard. It can still be high consequence if a serious third-party injury or vehicle claim occurs.

If your business has any of the following, commercial umbrella insurance deserves a serious review:

| Question | Why it matters |

|---|---|

| Do clients or landlords require higher limits? | Contractual requirements often force the issue before claims do |

| Do employees drive on company business? | Auto losses can escalate quickly |

| Do people visit your office or worksite? | Premises injuries create third-party liability exposure |

| Do you operate across multiple states? | Coverage planning gets more complex as operations spread |

| Would one severe claim disrupt cash flow or growth? | That is the core financial test |

Practical view: The businesses most likely to overlook umbrella coverage are often the ones that think of themselves as “not risky.” That label does not help if a contract requires higher limits or a severe claim exceeds the base program.

Commercial umbrella insurance is usually sold in $1 million increments. That sounds simple. Buying it is not.

The practical challenge in 2026 is that owners are shopping in a market where pricing, available limits, and underwriting appetite have all tightened. So if a renewal quote feels higher than expected, that may reflect market reality more than anything unique about your business.

By 2025, commercial umbrella costs had tripled in some sectors, with lead carriers reducing offered limits from $25 million down to $5 million to $15 million per policy. SMBs may also face 20% to 300% renewal increases, according to World Insurance’s analysis of rising umbrella and excess liability costs.

For a small business owner, that shows up in three ways:

Umbrella underwriters are not just pricing one isolated policy. They are evaluating the whole liability picture.

They typically review:

One of the key underlying lines in that conversation is employer’s liability insurance, because severe employee-related claims that fall outside the standard workers’ compensation framework can move into that part of the liability program.

Owners often ask a fair question: should we buy more umbrella or keep the premium down?

The answer depends on what problem you are solving.

If the issue is contract compliance, the limit has to satisfy the contract. If the issue is catastrophic protection, the limit should reflect the size of loss the business cannot comfortably absorb.

That may lead to an uncomfortable conclusion. The cheapest option is not always the usable option.

Treat umbrella pricing like a capital preservation decision, not a commodity purchase.

A low quote can still be expensive if it comes with narrow terms, lower available limits, or a carrier that forces awkward layering late in the renewal process. A more expensive quote can still be the better buy if it aligns cleanly with the underlying program and avoids coverage friction.

The easiest way to understand commercial umbrella insurance is to look at the kinds of claims that can pierce the base layer.

Not every claim does. Most do not. Umbrella coverage exists for the losses that are infrequent, severe, and financially disruptive.

An employee is driving to a client site and causes a serious multi-vehicle accident.

The commercial auto policy responds first. If injuries are severe and multiple parties are involved, the claim can outgrow the underlying auto limit. That is where the umbrella layer can matter. It helps protect the business from having a large unpaid balance after the auto policy has done all it can.

Auto claims deserve close attention because pricing pressure and loss severity have both been difficult for employers. For context on that broader environment, see why commercial and personal auto insurance rates are rising.

A client slips in your office lobby, suffers a permanent injury, and alleges unsafe conditions.

General liability responds first. If the injury is severe and legal costs mount, a standard liability limit may not be enough. A properly structured umbrella policy can sit above that general liability coverage and provide additional protection.

This is one reason low-risk office businesses should not dismiss umbrella coverage too quickly. A polished office does not eliminate premises liability.

A marketing campaign leads to a libel or slander allegation. The claimant argues that reputational damage caused serious financial harm.

If that type of allegation is covered under the underlying general liability policy and the claim grows beyond the base limit, umbrella coverage may extend above it. The important phrase is “if covered.” This is not automatic. It depends on how both the underlying and umbrella forms are written.

Key point: Umbrella policies help with severity. They do not turn an excluded claim into a covered one.

Owners can encounter problems when commercial umbrella insurance is powerful, but not universal.

Common exclusions or non-covered areas often include:

Do not buy umbrella coverage assuming it fills every gap in your program.

Instead, ask a more disciplined question: which severe third-party liability claims could hit our business, and which policies are designed to respond? That question produces a much better insurance program than chasing high limits alone.

The hardest part of buying commercial umbrella insurance is not deciding whether you need it. It is confirming that the policy you buy will work the way you think it will.

That takes more than reviewing premium and limit.

Most commercial umbrella policies are stand-alone with custom-drafted forms, not follow-form as many buyers assume. That means they can have their own insuring agreements and exclusions, which can create significant coverage gaps if not carefully compared against the underlying general liability, auto, and employer’s liability policies, according to IRMI’s commentary on commercial umbrella policy structure.

That distinction matters more than most buyers realize.

A follow-form structure generally mirrors the underlying policy more closely. A stand-alone structure may define covered loss, exclusions, notice requirements, and other terms independently. On a quote sheet, both can look acceptable. In a claim, they can behave very differently.

Use a checklist that forces real comparison, not just a premium decision.

Your umbrella should attach where your underlying policies stop. If the policy language is vague, you may discover a gap only after a claim.

Do not assume the umbrella adopts the underlying policy’s wording. Review exclusions for auto, employment-related liability, contractual liability, and personal and advertising injury.

Do not settle for a casual verbal answer. Ask for the specific form language and have your advisor explain the practical difference.

An umbrella policy only works properly if the correct underlying policies and limits are listed. If a relevant underlying line is missing or mismatched, the structure can fail where you need it most.

Buying advice: If the proposal arrives late in the renewal cycle, resist the urge to skim. Umbrella policies often look similar on the first page and differ sharply in the wording that follows.

What works is a side-by-side review of the underlying and umbrella forms, with attention to attachment, exclusions, and scheduled policies.

What does not work is treating umbrella insurance like a commodity add-on. That approach saves time right up until a serious claim tests the language.

Commercial umbrella insurance gets better when it is part of an integrated risk process rather than a last-minute purchase.

That is where a PEO relationship can help. The value is not only administrative convenience. It is the ability to view insurance, payroll, HR, safety, and claims through one operating lens.

A PEO sees the business in motion.

Payroll data, employee counts, job roles, onboarding practices, safety concerns, workers’ compensation activity, and multi-state employment issues all shape the liability profile. That broader context helps leadership make a better decision about whether the company needs umbrella coverage, how much it may need, and which underlying lines should be reviewed before shopping the market.

For companies evaluating a professional employer organization, that integrated view is one of the most practical advantages. The business is not trying to piece together risk insights from disconnected vendors.

Umbrella quoting often happens late because the underlying program has to be finalized first. That creates rushed review, weak comparison, and a higher chance of buying on price alone.

A strong PEO process reduces that scramble.

It can help the employer organize payroll details, classify operations accurately, identify employee driving exposure, and surface contract requirements early enough to build a cleaner renewal strategy. That does not guarantee the lowest premium. It does improve the odds of a better-structured result.

A major liability claim is operationally disruptive even before it becomes financially disruptive.

Owners have to preserve records, coordinate with carriers, communicate internally, and keep the business running while the claim moves through the primary and potentially umbrella layers. Having a knowledgeable team involved can reduce confusion at the exact moment when confusion is most expensive.

Small and midsize businesses usually do not have an in-house risk manager reading umbrella forms line by line.

They still face the same insurance market, the same contractual pressure, and the same need to respond correctly when a claim hits. An integrated partner helps close that expertise gap.

Bottom line: The primary advantage is not that a PEO makes umbrella insurance simple. It is that a PEO helps prevent oversights that become expensive later.

No. Commercial umbrella insurance is a liability policy. It is designed for covered third-party claims, not damage to your own building, equipment, or contents.

Not always. They are related, but they are not interchangeable.

| Feature | Commercial Umbrella Insurance | Excess Liability Insurance |

|---|---|---|

| Scope | Usually sits above multiple underlying liability policies | Usually extends the limit of one specific underlying policy |

| Coverage approach | May provide broader protection in some situations, subject to policy wording and any SIR | Typically follows the underlying policy’s scope more narrowly |

| Common use | Businesses that want one added layer across several liability lines | Businesses that need more limit on a single line |

| Key review point | Attachment, exclusions, SIR, and whether the form is stand-alone or follow-form | Which exact policy it sits over and whether it is true follow-form |

Maybe, but “low risk” is not the only test. Contract requirements, employee driving, office visitors, and multi-state operations can all justify umbrella coverage even for white-collar firms.

Usually not. Professional liability exposures such as consulting errors, design mistakes, or service failures generally need separate E&O coverage.

Review it before renewal, before signing major contracts, when adding locations, when employees begin driving more often for work, and when expanding into new states.

Don’t wait until your primary coverage runs out to find out you’re exposed.

Make sure your business has the protection it needs before a major claim happens.

👉 Talk to a Helpside expert today to review your coverage and see if an umbrella policy is right for you.

Call Helpside today for your Free 15-Minute Benefits Audit: 1-800-748-5102

Further Readings:

What Is a Professional Employer Organization (PEO)?

Why Small Businesses Plateau (And How a PEO Fixes It)

Why Onboarding with a PEO Can Make or Break Your Business Growth

If your team is growing and your insurance program feels fragmented, Helpside can help you connect payroll, HR, benefits, workers’ compensation, and risk management in one place. Learn more about Helpside and see how a more integrated approach can reduce administrative strain while helping you make smarter coverage decisions.