Services

Payroll, benefits, HR, and risk management in one PEO solution.

You promised a new hire a clean bonus amount. Payroll ran it like any other supplemental payment. The employee opens their bank app, sees less than expected, and asks why the company changed the deal.

That moment is where grossed up for taxes becomes practical, not theoretical.

For small businesses, the issue gets harder fast. A one-time bonus in one state is manageable. A relocation reimbursement for an employee moving into Utah, Idaho, Arizona, or Wyoming is not. Add different state tax rules, payroll taxes, and reporting requirements, and a simple promise can turn into a compliance problem if the math is off.

Grossing up for taxes means increasing a taxable payment so the employee receives a specific net amount after withholding.

For a small business with employees in more than one state, that decision affects more than a single paycheck. A gross-up changes employer cost, payroll tax withholding, reporting, and sometimes the employee conversation after the payment hits their account. If you have people in Utah, Idaho, Arizona, or Wyoming, the state piece may be simple in one case and more involved in the next, especially if the payment is tied to relocation, a sign-on bonus, or a one-time award.

This distinction matters.

If you tell an employee, “We’re giving you a $10,000 net relocation payment,” payroll cannot process $10,000 as wages directly and hope the withholding works out. The company has promised what the employee will keep, not what the company will pay.

The standard formula is:

Gross amount = Net amount ÷ (1 – total tax rate)

Using a desired net payment of $10,000 and a combined tax rate of 35%, the grossed-up total is $15,384.62. In that case, the employer adds $5,384.62 so the employee nets the intended amount after taxes.

The practical issue is cost control. Owners often approve the net amount first, then realize later that the true company cost is much higher once federal withholding, FICA, and any state or local taxes are included. That is one reason it helps to understand the full set of employer payroll tax responsibilities before you commit to a net payment in an offer letter or reimbursement policy.

Employers usually use gross-ups because they want the company to absorb the tax cost of a taxable payment.

Common examples include:

For a business with 20 to 150 employees, gross-ups are often less about theory and more about consistency. If one Arizona employee is told a bonus is “net” and another Idaho employee gets a gross amount with normal withholding, payroll ends up cleaning up a policy problem, not just a calculation problem.

Practical rule: If the company promises a net result, payroll has to build the gross amount to support it.

A gross-up includes a tax-on-tax effect. The extra wages added to cover withholding are also taxable wages.

That is where small errors turn into expensive ones. If the estimate is too low, the employee receives less than promised. If the estimate is too high, the company pays more than it budgeted. In a multi-state workforce, the gap gets wider because state withholding rules do not always line up neatly with a flat federal assumption.

I see this most often with relocation payments and off-cycle bonuses. The manager focuses on the promised amount. Payroll then has to determine which taxes apply, which state should source the wages, and whether the payment will be processed with regular payroll or as supplemental wages. Those details change the result.

There is also a compliance issue. Employers are required to withhold, deposit, and report payroll taxes correctly. The IRS explains the trust fund recovery penalty under IRC Section 6672, which can apply to responsible persons when withheld employment taxes are not properly paid over. Gross-ups do not create new payroll tax rules, but they do raise the stakes if payroll is handled casually.

A gross-up is still taxable compensation. It does not remove the tax. It shifts the tax cost from the employee to the employer.

That makes gross-ups useful, but not automatic.

For many small businesses, the better question is whether the payment needs to be net at all. If the purpose is recruiting or making an employee whole during a move across state lines, a gross-up can make sense. If the payment is discretionary and the company has employees working in several states with different withholding variables, a standard gross payment may be cleaner, easier to explain, and less likely to create follow-up corrections later.

A Utah employer promises a new hire a $500 net sign-on bonus. Payroll can get that done in a few minutes if the employee works only in one state and the company accepts a small variance. The calculation gets harder fast if that same employee lives in Idaho, works part of the time in Utah, or receives the payment alongside other wages that change withholding.

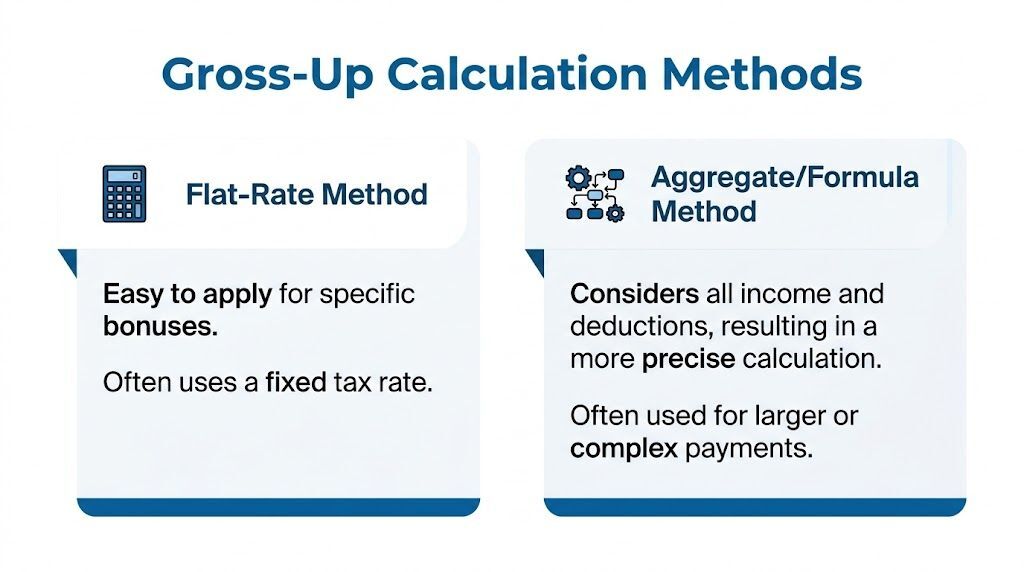

Most small employers end up using one of two methods. One is faster to run. One gives a truer net result.

The flat-rate method applies a single combined tax rate to estimate the gross payment needed to deliver a target net amount.

Payroll teams use it because it is quick and easy to explain. For a straightforward off-cycle bonus, that can be enough. A common example is a $500 net target using a combined rate made up of 22% federal supplemental withholding, 6.2% Social Security, and 1.45% Medicare. Using that approach, the gross-up is:

$500 ÷ (1 – 0.2965) = $710.73

That math is clean. Real payroll is not always that clean.

For 2026 planning, use current rates and wage bases in your payroll system rather than carrying forward older examples from prior years. If you use a prior-year illustration internally, label it clearly as an example so managers do not treat it as a live tax setup.

Flat-rate gross-ups break down when the employee’s actual tax picture differs from your standard assumption. That happens often in growing companies with employees across Utah, Idaho, Arizona, and Wyoming. Arizona has state income tax withholding. Wyoming does not. Idaho and Utah add their own withholding rules and employee form inputs. If you use one blended rate across all four, someone is likely to be over-grossed or under-grossed.

That matters for cost control as much as employee relations. A small miss on one payment is manageable. Repeat that error across several hires, relocations, or executive bonuses, and your payroll tax cost rises faster than expected.

The inverse method works backward from the net amount the employee must receive and recalculates the taxable wages until the taxes and net pay align.

This is the method I recommend when the promise to the employee is specific. If an offer letter says the employee will receive a net relocation payment or a true net sign-on bonus, payroll should calculate to the promised result, not to a rough estimate.

In practice, payroll systems and spreadsheets solve this through repeated recalculation. The gross payment increases, taxes are recomputed, and the process repeats until the net lands where it should. It takes longer than a flat-rate estimate, but it reduces cleanup later.

Small businesses with 20 to 150 employees often hit an awkward stage. They are large enough to hire across state lines, but not large enough to absorb repeated payroll corrections without feeling it.

A single gross-up can involve federal supplemental withholding, FICA taxes, state withholding, local rules in some jurisdictions, and wage-base timing. Add an employee who moved mid-year or works in one state and lives in another, and the wrong method can create three separate problems. The employee gets the wrong net amount. Payroll reporting needs correction. The company spends more than it budgeted.

That is why process matters. The best payroll teams do not just pick a formula. They confirm work state, residence state, payment type, wage-base status, and whether the payment is being run separately or with regular wages. If your team needs a refresher on those tax mechanics, review this guide to employer payroll tax rules and calculations.

| Method | Best For | Accuracy | Complexity |

|---|---|---|---|

| Flat-rate method | Routine one-time payments with standardized treatment | Moderate | Low |

| Inverse method | Relocation, multi-state payments, and payments tied to a promised net amount | High | Higher |

Use the flat-rate method when the payment is simple, the stakes are low, and your policy allows a reasonable estimate.

Use the inverse method when the employee was promised a specific net amount, the payment crosses state lines, or the cost of getting it wrong is higher than the time it takes to calculate it correctly.

For many small businesses, that second category comes up more often than expected.

A gross-up decision usually gets tested the moment an employee asks a simple question: “Why didn’t I receive what I was promised?”

For small businesses with employees across Utah, Idaho, Arizona, and Wyoming, that question comes up in predictable places. Bonuses promised as a net amount. Relocation reimbursements tied to a cross-state move. Awards that look generous until withholding hits the paycheck.

A common example is a hiring or retention bonus that was discussed in net terms. If you promise a new manager a $500 take-home bonus, payroll cannot treat $500 as the gross payment and hope it lands close enough. Withholding will reduce it, and the employee will notice.

The fix is straightforward. Gross up the payment so the employee receives the intended net amount after withholding. That matters even more when your workforce spans multiple states, because the total tax impact may differ based on work location, residency, and any local withholding rule that applies.

This issue often starts before payroll sees the payment. Recruiting says “$500 bonus.” Finance budgets for $500. Payroll has to explain why the actual employer cost is higher. Keeping those teams aligned early saves rework later. This guide to understanding bonus pay for employers helps set that expectation.

If you are reviewing systems and processes around one-time payments, your payroll workflow also needs to tie cleanly into the best accounting software for small business so bonus expense, tax cost, and reimbursement entries stay consistent.

Relocation is where gross-ups get expensive fast.

Because most relocation expenses are now taxable under current law, many employers choose to gross up those payments so the employee is not left covering taxes on a move the company requested. That sounds simple until the employee moves from Arizona to Utah mid-year, or lives in one state while working in another.

In practice, small employers often overlook the full cost. The reimbursement itself is only part of the budget. The gross-up adds employer cost, and state treatment can shift the total again depending on where the wages are sourced and when the payment is made. A move package that looked manageable in an offer letter can cost far more once payroll applies all required withholding.

Clear policy language prevents most disputes. If your offer says you will reimburse moving costs, say whether the reimbursement is taxable, whether you will gross it up, and whether there is a cap. Without that detail, employees often assume the company will make them whole.

Awards create a different problem. The company intends to recognize strong performance, but the tax treatment can undercut the message.

A company-paid trip, a high-value gift, or another taxable award may increase wages even if no cash changes hands. If the business wants the employee to enjoy the full value of the award, payroll may need to gross up the tax effect. If not, the employee may see lower net pay on the next check and connect that reduction to the award.

I see this most often with fast-growing employers that run payroll in more than one state and process awards outside their normal compensation cycle. The taxable value is identified late, the gross-up question is asked after payroll is finalized, and corrections follow.

A cleaner process is simple:

Gross-ups are not just a tax calculation. They are a policy decision about who should bear the tax cost.

For a 20 to 150 person business, that decision should be deliberate. Grossing up every bonus or award can inflate payroll costs quickly. Refusing to gross up relocation or promised net bonuses can damage trust, especially when employees cross state lines for the job. The right answer depends on the promise you made, the states involved, and whether the business is prepared for the full employer cost.

A gross-up can look finished when the net check lands where you wanted it. The critical test comes later, when payroll has to report it correctly across the employee record, tax filings, and year-end forms.

That is where small employers with teams in Utah, Idaho, Arizona, and Wyoming feel the strain first. A payment that looked straightforward in one state can require different withholding treatment in another, especially when an employee lives in one state and works in another or moves mid-year.

Clean reporting starts with visibility. If an employee receives a grossed-up bonus, relocation payment, or taxable award, the payroll record should show the underlying payment and the added wages used to cover tax withholding.

A usable audit trail should make four things easy to confirm:

Employees notice this too. If the pay stub only shows a larger wage amount with no clear explanation, payroll gets the call.

The biggest errors are rarely math errors. They are setup and sourcing errors.

For small businesses with 20 to 150 employees, a gross-up often gets approved by one person, entered by another, and reviewed after the payroll is already processed. Add one remote employee in Idaho, a relocated manager in Arizona, and a sales rep working from Wyoming, and a single standard worksheet stops being reliable.

Common failure points include:

For employers working through those issues, this guide to multi-state payroll laws what employers will need to know is a useful reference alongside your gross-up policy.

Multi-state gross-ups affect more than employee net pay. They also change employer tax cost, workers’ compensation payroll, benefit-related wage reporting, and general ledger cleanup if the entry is wrong.

That matters for small businesses watching margins closely. A relocation gross-up for an employee moving into Utah may cost the company something very different than the same promise made to an employee in Wyoming, where there is no state income tax. If the business budgets one flat percentage for both, finance will either come up short or overfund the payment.

That is one reason many owners review payroll workflows at the same time they review the rest of the finance stack. If payroll data does not post cleanly into your books, reconciliations get messy fast. Many compare their systems against guides to the best accounting software for small business so payroll entries, tax liabilities, and reporting stay aligned after each run.

A reliable process usually includes state-aware payroll settings, one approval path for exceptions, and a final review before the payment is released. The goal is consistency.

I advise small employers to treat any cross-state gross-up as a higher-risk payroll item. Confirm the taxable treatment first. Confirm which jurisdictions apply. Then run the payment through a system that can handle the withholding logic instead of forcing payroll staff to recreate it by hand.

These practices hold up well as headcount and state complexity increase:

If a payment crosses state lines, the formula is only part of the job. Reporting and withholding determine whether the gross-up works.

Most gross-up mistakes don’t happen because a company meant to cut corners. They happen because the payment looked simple at the start.

The risks show up later in under-withholding, inconsistent treatment, and confused employees.

The common shortcut is to pick one percentage and move on.

That can work for routine payments, but it often underpays when the gross-up itself creates added tax. Under SEC-related disclosure rules, employers must disclose employee tax gross-ups that exceed $10,000 annually, while amounts below that threshold avoid enhanced scrutiny, as outlined in this explanation of gross-up disclosure rules and method trade-offs.

What to do instead: Reserve flat-rate gross-ups for lower-risk, standardized payments. Use a more precise method for executive compensation, relocation, severance, or anything promised as a true net amount.

One leader approves a gross-up for a new hire. Another denies it for a similar employee. Payroll is left to process exceptions without a policy.

That creates morale problems first. It can also create legal risk if the pattern suggests uneven treatment among similarly situated employees.

What to do instead: Put eligibility in writing. Define which categories of payment can be grossed up, who approves them, and when exceptions are allowed.

Employees often don’t understand that the company paid extra so they could receive the intended value.

If the pay statement isn’t clear, the employee may think the company over-withheld or changed the deal.

What to do instead: Tell the employee in advance that the payment is being grossed up, explain that the gross-up itself is taxable, and make sure payroll records reflect the calculation clearly.

A company may have a solid federal calculation and still get the payment wrong because it overlooked state-specific treatment.

This gets worse as companies expand into multiple jurisdictions. The error may not be obvious until quarter-end or year-end reporting.

What to do instead: Treat every multi-state gross-up as a separate compliance event. Review withholding assumptions before payroll runs, not after.

Yes, but the decision should follow a written policy and a defensible business reason.

Common reasons include relocation support, executive agreements, or sign-on packages for hard-to-fill roles. What matters is consistency within each category.

If a prize or award has a clear taxable value, payroll can include that value in wages and then decide whether to gross up the related taxes.

The key is documenting the value, communicating the tax treatment, and processing it through payroll rather than treating it as an informal perk.

In many situations, no. It’s usually a business choice, not a legal mandate.

The legal requirement is to withhold, report, and remit payroll taxes correctly when a payment is taxable. The gross-up decision is about who bears that tax cost.

A gross-up usually addresses a specific taxable payment so the employee receives a target net amount.

Tax equalization is a broader policy framework often used in international assignments. It tries to keep the employee in a neutral tax position across jurisdictions, which is a more complex design issue tied to broader strategic financial planning, compensation policy, and mobility administration.

Call Helpside today for your Free 15-Minute Benefits Audit: 1-800-748-5102 and see how much time and money your business could save.

Further Readings:

If grossed up for taxes is starting to show up in your bonus plans, relocation packages, or multi-state payroll runs, this is usually the point where a clean process pays for itself. Helpside works with growing employers that need payroll, HR, benefits, and compliance support without stitching together separate vendors.