Services

Payroll, benefits, HR, and risk management in one PEO solution.

Learning how to do payroll really comes down to a few foundational steps: getting the right tax ID numbers, collecting the essential employee paperwork, and picking a consistent pay schedule. Getting these administrative tasks right from the start is the single most important thing you can do to prevent costly compliance headaches down the road.

Before you can pay your first employee, you have to get your legal and administrative house in order. Think of it as laying the foundation for your business—any cracks here will cause major problems later on. This initial setup makes sure you can accurately calculate pay, withhold the correct taxes, and report everything to the right government agencies.

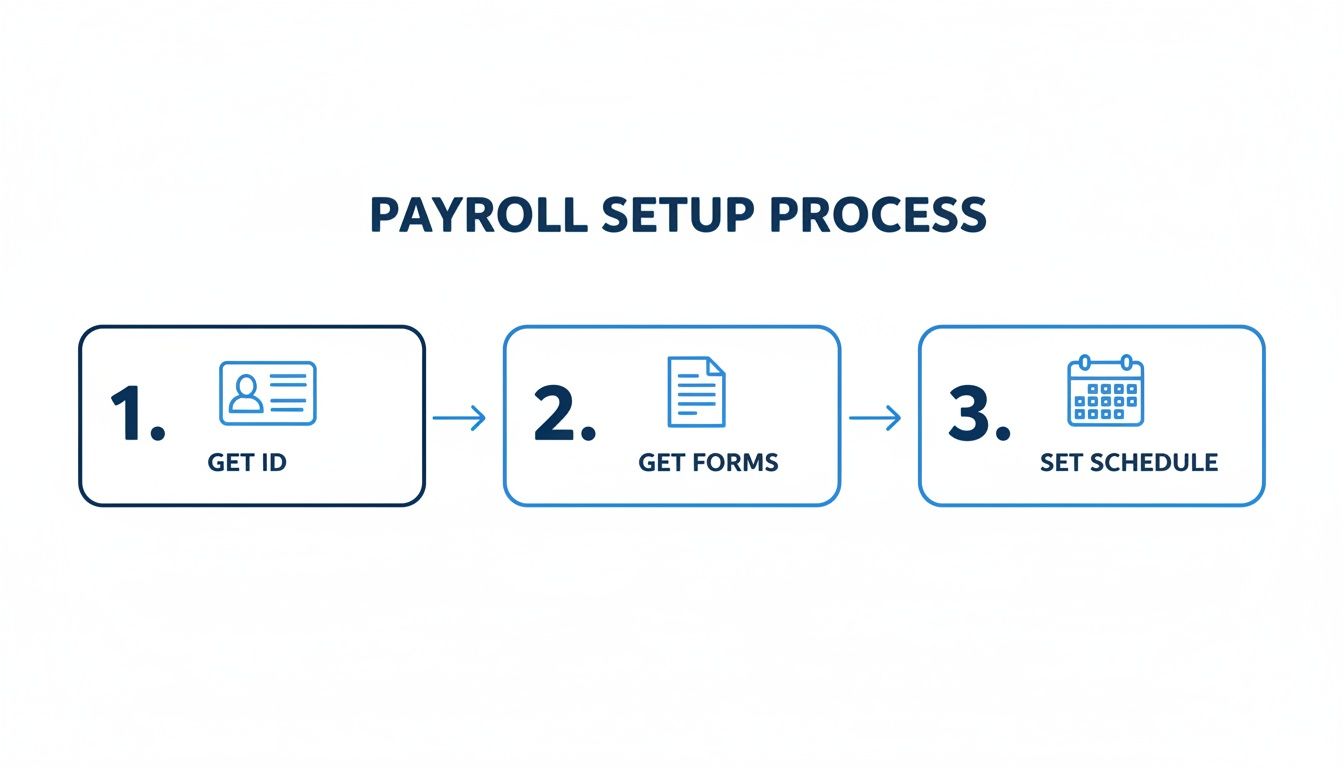

The whole process boils down to gathering your IDs, collecting forms, and setting your payment rhythm.

As you can see, these first few tasks create the legal and operational structure you need before any money changes hands, ensuring you’re compliant from day one.

Your very first move is to apply for a federal Employer Identification Number (EIN) from the IRS. It’s a free service, and this number acts like your business’s Social Security Number for all federal tax matters. You simply cannot legally hire and pay employees without it.

Beyond the federal EIN, you’ll also need to register with your state and sometimes local tax agencies. Each state has its own system for unemployment insurance taxes and, in most cases, income tax withholding. For example, businesses in Utah register with the Utah State Tax Commission for withholding tax and the Department of Workforce Services for unemployment insurance. Arizona employers, on the other hand, register with the Arizona Department of Revenue and the Department of Economic Security. These state-specific IDs are mandatory for remitting the taxes you withhold and paying state unemployment taxes.

Once you have your tax IDs, you can start onboarding employees. This means collecting two crucial pieces of documentation from every single new hire.

Key Takeaway: Handling these forms correctly is absolutely non-negotiable. Mishandling sensitive employee data or failing to verify employment eligibility carries significant legal and financial risks. You need a secure, confidential system for storing this information from the very beginning.

To help you stay on track, here’s a quick checklist of these essential setup tasks.

This table summarizes the foundational tasks you must complete before running your first payroll. Getting these right is critical for compliance.

| Task | What It Is | Why It Is Critical |

|---|---|---|

| Get Federal EIN | Your business’s unique 9-digit tax ID from the IRS. | You cannot legally hire, pay, or file payroll taxes without it. |

| Register for State IDs | State-specific numbers for income tax withholding and unemployment insurance. | Required for remitting state taxes and reporting wages. |

| Collect Form W-4 | An IRS form where employees declare their tax withholding allowances. | Determines the correct amount of federal income tax to withhold from each paycheck. |

| Collect Form I-9 | A USCIS form used to verify an employee’s identity and right to work in the US. | A mandatory federal requirement to ensure a legal workforce. |

Nailing this checklist ensures your payroll system has a solid, compliant foundation.

Next up, you need to decide how often you’re going to pay your team. This is your pay schedule. Common options include weekly, bi-weekly (every two weeks), semi-monthly (twice a month), and monthly. Your choice will affect your cash flow and must follow state law, as many states mandate minimum pay frequencies. For example, Arizona requires employers to pay employees at least twice a month, not more than 16 days apart.

At the same time, it’s vital to classify your employees correctly. Understanding the difference between an exempt vs nonexempt employee is fundamental, as this determines their eligibility for overtime pay under the Fair Labor Standards Act (FLSA). Misclassifying an employee can lead to expensive back pay and penalties.

Finally, a mandatory and crucial step is new hire reporting. Federal law requires employers to report new and rehired employees to a designated state agency shortly after they start. This information is primarily used to enforce child support orders. Deadlines and reporting methods vary significantly by state, so it is critical to check your state’s specific requirements.

If these foundational tasks already feel a bit overwhelming, you’re not alone. Many small business owners find it helpful to learn about ways to make small business payroll easier.

Once your payroll system is in place, the real work begins with calculating gross pay. This is the total amount an employee earns before any taxes or deductions are taken out, and getting it right is the bedrock of an accurate paycheck.

The way you calculate this number comes down to one key difference: whether your employee is salaried or hourly.

For salaried employees, calculating gross pay is usually straightforward. These team members earn a fixed annual salary, regardless of the specific hours they log in a given week.

To find their gross pay for any pay period, you just divide their annual salary by the number of pay periods in the year.

For an employee with a $65,000 annual salary, the math looks like this depending on your pay schedule:

While this consistency makes things easier, don’t fall into the trap of thinking “salaried” automatically means “exempt from overtime.” An employee’s job duties and salary must meet specific Fair Labor Standards Act (FLSA) criteria to be truly exempt from overtime.

Calculating gross pay for hourly employees demands careful time tracking. Their earnings are the total hours worked in a pay period multiplied by their hourly rate. This has to account for regular time, overtime, and sometimes even other special pay rates.

The FLSA requires that most hourly (non-exempt) employees get paid 1.5 times their regular rate for any hours they work over 40 in a single workweek. Some states, like California, Alaska, and Nevada, have even stricter rules, such as daily overtime.

When you’re figuring out gross pay for your hourly team, you have to nail the overtime, especially with complex state laws like those explaining how to calculate overtime in California.

Real-World Scenario: An employee earns $20 per hour and works 45 hours in one week.

- Regular Pay: 40 hours x $20/hour = $800

- Overtime Rate: $20/hour x 1.5 = $30/hour

- Overtime Pay: 5 hours x $30/hour = $150

- Total Gross Pay: $800 + $150 = $950

This calculation can get even trickier in states that mandate daily overtime or double-time pay. It’s why having a rock-solid timekeeping system is an absolute must.

Gross pay isn’t just about regular hours and overtime. To stay compliant and pay your team correctly, your math has to include all other forms of compensation they’ve earned.

Paid Time Off (PTO), Sick Leave, and Holidays

When an employee uses their PTO, takes a sick day, or gets paid for a company holiday, that time needs to be added to their gross pay. For hourly employees, this time is almost always paid at their regular hourly rate.

Variable Pay: Commissions and Bonuses

For salespeople or other roles driven by performance, commissions and bonuses are a huge part of their paycheck.

Getting this wrong can throw off your overtime calculations and open you up to serious compliance risks. Every dollar an employee earns, from a sales commission to holiday pay, must be part of their total gross pay.

Once you have an employee’s gross pay figured out, you need to get to their net pay—the actual amount that lands in their bank account. This is the number your employees are watching, and the journey from gross to net is filled with crucial deductions.

These subtractions fall into three main buckets: mandatory taxes, voluntary benefits the employee chooses, and involuntary garnishments. Each comes with its own set of rules, and handling them correctly is non-negotiable for staying compliant.

Every single employer in the U.S. is legally required to withhold certain taxes from employee paychecks. These aren’t optional—they form the foundation of payroll deductions.

The main mandatory deductions are:

It’s vital to know the difference between employer-paid payroll taxes and the income taxes withheld from employees. If you need a deeper dive, you can learn more about how payroll taxes and income taxes differ in our in-depth article.

Beyond taxes, employees can also elect to have money withheld for various benefits. We call these voluntary deductions because the employee is opting in. Offering a solid benefits package is one of the best ways to attract and keep great people.

These deductions can also have a big impact on an employee’s taxable income, depending on whether they are pre-tax or post-tax.

Pre-Tax vs. Post-Tax Deductions Explained

This table breaks down how each type works and how it affects an employee’s final paycheck.

| Deduction Type | How It Works | Common Examples |

|---|---|---|

| Pre-Tax | Deducted from gross pay before income taxes are calculated, which lowers taxable income. | Health insurance premiums, 401(k) contributions, Health Savings Account (HSA) funds. |

| Post-Tax | Deducted from net pay after all taxes have been calculated. This does not reduce taxable income. | Roth 401(k) contributions, disability insurance, charitable donations. |

Real-World Impact: Imagine an employee earns $2,000 in gross pay and contributes $100 pre-tax to their 401(k). Their taxable income for federal and most state purposes drops to $1,900. This means they pay less in income tax for that pay period, which directly increases their take-home pay while they save for retirement.

Getting benefit deductions right is just as critical as handling taxes. One small mistake could cause an employee to lose their health coverage or miss out on retirement contributions.

The last category of deductions is completely out of your employee’s control. These are wage garnishments—involuntary deductions ordered by a court or government agency. As an employer, you are legally obligated to comply.

Common examples include:

Handling garnishments is a high-stakes responsibility. Both federal and state laws dictate exactly how much you can withhold, the proper order for paying multiple garnishments, and how to send the funds. If you fail to comply, you—the employer—can face severe penalties, not just the employee.

Because the rules are so strict and the consequences so serious, managing garnishments is one of the top reasons business owners look for expert payroll support. It’s an area where a single misstep can lead to legal headaches and erode employee trust.

Getting the paychecks calculated correctly is a huge step, but you’re not quite at the finish line. That money you withheld from your employees, plus your own employer tax contributions, needs to be sent to the right government agencies. And they have a very strict schedule.

This is where a lot of businesses get into serious trouble. Timely tax deposits and accurate reporting are just as critical as the payroll calculations themselves. The IRS and state agencies don’t mess around with missed deadlines—penalties and interest can pile up fast enough to cripple a small business.

After every payroll, you’re holding a pool of money that includes federal income tax, Social Security, and Medicare you withheld from employees, along with your matching share of FICA. Your next job is to deposit those funds with the U.S. Treasury. The IRS will tell you how often you need to do this by assigning you a deposit schedule. It’s either monthly or semi-weekly, and it’s based on your total tax liability from a prior “lookback period.”

Most new businesses will start out as monthly depositors. But as you grow and your tax liability increases, the IRS will bump you up to the more frequent semi-weekly schedule.

Expert Tip: Whatever you do, never use payroll tax funds to cover other business expenses. The IRS views this as a major offense. That money is held in trust for your employees and the government, and failing to remit it can lead to severe penalties, including personal liability for business owners.

Depositing taxes is how you pay; filing reports is how you show your work. These forms are how you reconcile your payments with the government, detailing exactly how much you paid in wages and how much tax you collected and sent in.

For the federal government, these are the main forms you’ll get to know:

When the calendar year wraps up, a few more critical reporting tasks pop up. This year-end process is a cornerstone of learning how to do payroll correctly, and it directly affects your employees and any contractors you worked with.

Issuing W-2s and 1099s

By January 31st each year, you are responsible for providing the following forms:

These forms are absolutely essential for people to file their personal tax returns. Getting them out late or with errors creates huge headaches for your team and can lead to penalties for your business. The administrative weight of all this reporting is a big reason why many growing businesses decide to outsource their payroll.

When you first started your business, handling payroll yourself likely made perfect sense. With just a handful of employees, a simple spreadsheet and a bit of focus got the job done.

But as your company grows, that once-manageable task can quickly become a major liability. The tipping point often arrives without you even realizing it.

Suddenly, you’re hiring your first out-of-state employee, dealing with a wage garnishment, or just spending way too much time chasing down timesheets instead of talking to customers. These are the classic growing pains that signal your DIY payroll process is no longer an asset but a risk. It’s a subtle shift from an administrative task to a strategic bottleneck.

The most obvious cost of doing payroll yourself is your time—hours that could be spent on sales, innovation, or team development. But the hidden costs are often far more damaging.

A single miscalculation on an overtime check or an error in tax withholding can ripple outward, leading to frustrated employees and time-consuming corrections. These aren’t just one-off mistakes. Each error erodes the trust you’ve built with your team. When paychecks are consistently wrong, it sends a message that the business is disorganized, which can hurt morale and even lead to turnover.

The complexity of payroll isn’t just a feeling; it’s a measurable global trend. The 2025 Global Payroll Complexity Index found that demands on payroll teams are intensifying, with average complexity scores rising by 5%. This environment makes it harder than ever for businesses to manage payroll effectively on their own, especially when 66% of payroll professionals don’t even have the tools to understand their banking and payment costs. You can discover more insights on this rising complexity.

Hiring your first employee in another state is a huge milestone. It’s also the moment your payroll complexity explodes. All at once, you’re not just dealing with federal and local laws—you have an entirely new set of rules to master.

We see this happen all the time. Here are a few common scenarios:

Trying to stay current with ever-changing tax laws across multiple states can feel like a full-time job. A single compliance slip-up can trigger audits, fines, and legal headaches that pull you away from your core mission.

For many leaders of growing businesses, the breaking point is clear: they are spending more time buried in administrative work than focusing on the vision that got them started. This is when shifting from a DIY approach to a strategic partnership becomes essential for sustainable growth. A Professional Employer Organization (PEO) can take on this burden.

This table highlights the key differences between managing payroll in-house and working with a PEO partner.

| Feature | In-House Payroll | PEO Partnership |

|---|---|---|

| Responsibility | You are solely responsible for all calculations, filings, and compliance. | The PEO assumes co-employment liability for payroll and tax compliance. |

| Technology | Requires you to purchase, learn, and maintain payroll software. | Access to an integrated, modern HR platform is included. |

| Expertise | You or your staff must become experts in multi-state tax and labor law. | You gain a dedicated team of certified payroll and HR professionals. |

| Risk | High risk of errors, penalties, and audits as complexity grows. | Mitigated risk through expert management and compliance oversight. |

Ultimately, the decision comes down to a simple question: Is managing payroll the best use of your time? If the answer is no, it’s a clear sign that DIY payroll is putting your business at risk. Businesses that partner with PEOs grow twice as fast and are 50% less likely to fail because they can focus on what they do best.

As your business grows, the administrative side of things—payroll, HR, and compliance—can quickly go from a minor task to a major headache. We’ve seen it happen time and again. What starts as a simple to-do list becomes a strategic burden, pulling your focus away from what really matters: growing the business.

This is where a Professional Employer Organization (PEO) comes in. It’s a common misconception that a PEO is just another payroll company. The reality is, a PEO is a strategic partner that helps manage the entire employee experience, from hire to retire. Through a co-employment model, you can offload these critical but time-consuming functions, freeing you up to focus on innovation and your core business.

A good PEO handles the entire web of employee management. It’s not just about running payroll correctly—it’s also about managing benefits administration, workers’ compensation, and tricky HR compliance issues. By bringing all these functions under one roof, you get a unified team of experts dedicated to your business.

This partnership becomes especially powerful when you start hiring across state lines. Instead of scrambling to become an expert in multiple states’ labor laws, you gain a team that already has that knowledge. They navigate the complexities for you, helping you sidestep compliance risks from day one.

The numbers really highlight this challenge. The 2025 Global Payroll Payments Report found that 61% of businesses name legal and regulatory compliance as their top payroll headache. It’s a problem that only gets bigger as you grow. You can learn more about these key business trends in the full report.

One of the biggest game-changers of a PEO partnership is gaining access to better, more affordable employee benefits. PEOs pool all their clients’ employees into one large group, giving them the collective buying power of a huge corporation.

This means your small or midsize business can suddenly offer the kind of benefits packages you’d expect from a Fortune 500 company, including:

In a tight labor market, offering high-quality benefits is no longer a perk—it’s a necessity. A PEO gives you a real competitive advantage in attracting and retaining the top talent you need to scale.

From workers’ compensation claims to creating a compliant employee handbook, a PEO provides a critical layer of protection for your business. They help you develop solid HR policies, manage tricky employee relations issues, and navigate the complexities of workplace safety and claims.

This expert oversight makes a huge difference. For instance, a PEO’s risk management specialists can help you implement safety programs that reduce workplace accidents, keeping your team safe and your insurance costs under control.

This proactive approach is one of the reasons that businesses partnered with a PEO are 50% less likely to fail. By offloading these high-stakes administrative tasks, leaders can focus on the strategic work that actually moves the needle. If you’re exploring this path, you might find it helpful to read about why partnering with a PEO is a smart move for businesses. Ultimately, it allows you to grow with confidence, knowing the people-side of your business is in expert hands.

Ready to stop worrying about payroll and start focusing on growth? At Helpside, we provide a dedicated team of HR, payroll, and benefits experts to support your business every step of the way. Discover how our PEO services can help you attract top talent, reduce administrative burden, and scale with confidence by visiting https://helpside.com to get started.