Services

Payroll, benefits, HR, and risk management in one PEO solution.

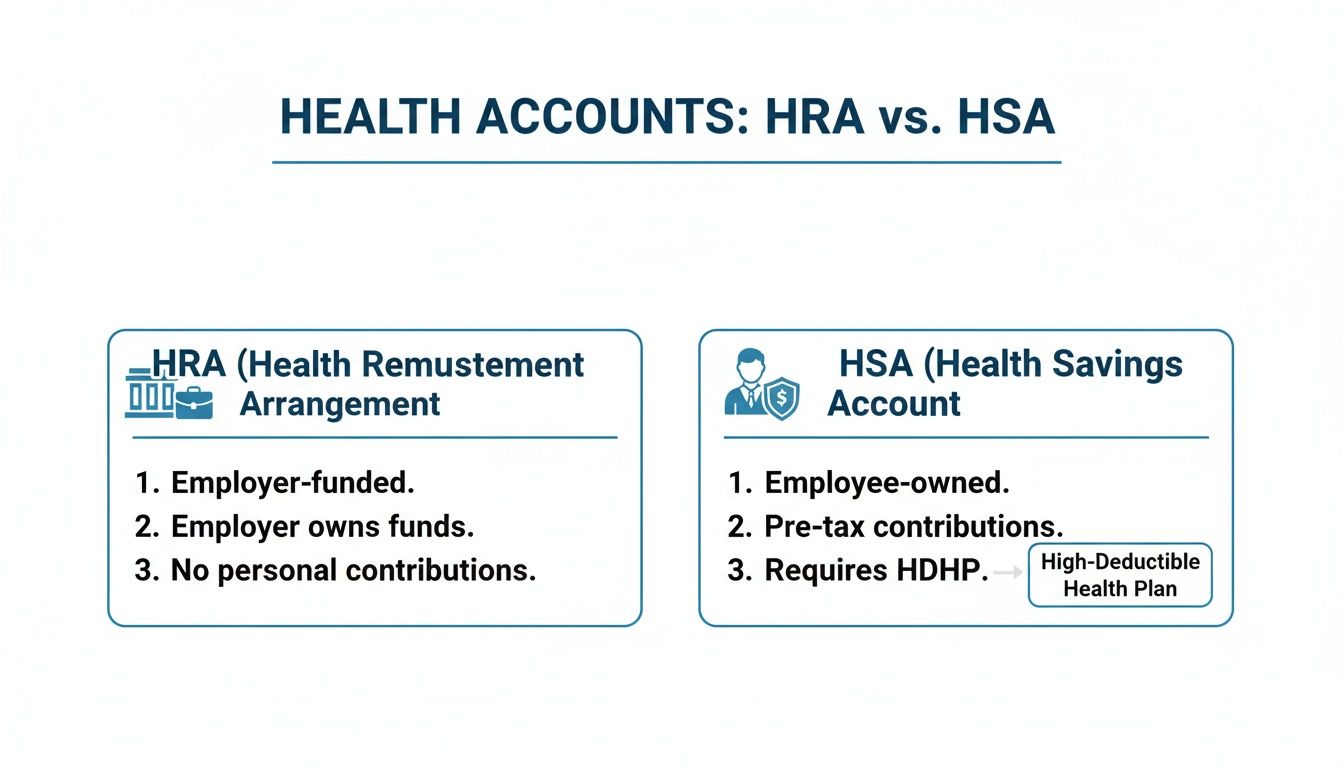

When you’re comparing an HRA to an HSA, the main difference really boils down to ownership and funding. A Health Reimbursement Arrangement (HRA) is an account owned and funded entirely by the employer. Think of it as a formal promise to reimburse employees for medical costs. In contrast, a Health Savings Account (HSA) is a tax-advantaged savings account owned and controlled by the employee, and it requires being paired with a specific type of insurance: a high-deductible health plan (HDHP).

Ultimately, an HRA gives you, the employer, more control over costs and plan design. An HSA, on the other hand, gives your employees a portable, long-term savings tool that they can take with them if they leave your company.

Choosing the right health benefits is one of the most significant decisions a small business owner can make. While both HRAs and HSAs help cover medical expenses with tax-advantaged money, they work in fundamentally different ways. Getting a clear handle on these distinctions is the first step toward building a benefits package that fits your company and your team.

An HRA isn’t a bank account. It’s a formal arrangement where you agree to reimburse employees for qualified medical expenses up to a specific dollar amount you set. The key takeaway here is that you only pay out what your employees actually use. Depending on the HRA design, any leftover funds at the end of the year may be forfeited back to the company, giving you predictable cost control.

An HSA is a completely different animal. It’s a true bank account owned entirely by the employee, which must be connected to an HSA-qualified high-deductible health plan (HDHP). Both you and your employee can contribute to an HSA, and the money belongs to the employee forever—even if they leave your company.

The primary distinction between an HRA and HSA comes down to a simple question: Who owns the money? With an HRA, the employer retains ownership of the funds. With an HSA, the employee owns the account and its balance outright.

This core difference really frames the conversation. An HRA is an employer-controlled benefit, while an HSA is an employee-empowering savings vehicle.

The image above gives you a quick visual, but let’s dig a little deeper into the specific features that will likely drive your decision.

This table breaks down the fundamental differences between Health Reimbursement Arrangements (HRAs) and Health Savings Accounts (HSAs) across key decision-making criteria for small businesses.

| Feature | Health Reimbursement Arrangement (HRA) | Health Savings Account (HSA) |

|---|---|---|

| Account Ownership | The employer owns the account and funds. | The employee owns the account and funds. |

| Who Can Contribute | Only the employer can contribute funds. | The employee, employer, or anyone else can contribute. |

| Portability | Funds are not portable and are forfeited if the employee leaves. | Funds are fully portable and stay with the employee for life. |

| Health Plan Requirement | Varies by HRA type; some require integration with a group or individual plan, while others have no plan requirement. | Must be paired with a qualified High-Deductible Health Plan (HDHP). |

| Tax Treatment | Employer reimbursements are generally tax-free to employees and tax-deductible for the employer. | Contributions are tax-deductible, funds grow tax-free, and withdrawals for medical expenses are tax-free (triple-tax advantage). |

While this covers the most critical points, the nuances between these accounts and another common option—the FSA—can get tricky. You can learn more by exploring the differences between HSAs, FSAs, and HRAs in our detailed guide.

This foundational knowledge will help you better assess which plan structure best aligns with your company’s financial goals and your overall employee benefits strategy.

While a Health Savings Account (HSA) is an employee-owned savings account, a Health Reimbursement Arrangement (HRA) is a completely different tool. Think of it less like a bank account and more like an employer-funded allowance designed for cost control and predictability.

The concept is simple. As an employer, you set a specific monthly or annual allowance for each employee. When an employee has a qualified medical expense, they submit proof, and you reimburse them up to their available balance. This means you only pay for the healthcare your employees actually use.

Critically, you, the employer, own all the funds. If an employee leaves the company or doesn’t spend their full allowance by the end of the plan year (and you don’t allow rollovers), the unused money goes right back to the business. This feature gives you a major advantage when it comes to managing and forecasting your benefits budget.

Unlike an HSA where the money belongs to the employee forever, an HRA is an employer-owned and funded benefit. Employees can’t contribute their own money. This gives you direct control over your financial commitment and how the plan is designed.

The tax advantages are a huge plus. Your reimbursements are 100% tax-deductible as a business expense, and the money your employees receive is income-tax-free for them, as long as they maintain qualifying health coverage as required by the specific HRA type.

However, this control comes with serious compliance duties. HRAs are governed by a complex web of regulations under the Affordable Care Act (ACA), ERISA, and the IRS. Navigating these rules requires careful administration to stay compliant and avoid significant penalties.

Not all HRAs are built the same. Federal regulations allow for several types, with two in particular offering modern, flexible benefits for small and midsize businesses.

Qualified Small Employer HRA (QSEHRA): This is for businesses with fewer than 50 full-time equivalent employees that do not offer a group health plan. A QSEHRA comes with annual contribution limits set by the IRS and must be offered on the same terms to all eligible full-time employees, though allowances can vary by family status.

Individual Coverage HRA (ICHRA): Available to businesses of any size, the ICHRA is arguably the most flexible HRA. It’s used to reimburse employees for individual health insurance premiums and other medical expenses. Critically, there are no federal contribution limits, giving you complete control over your budget.

The ICHRA also introduces a powerful strategic advantage for businesses with different types of employees. It allows you to create different allowance amounts for distinct employee classes.

An ICHRA’s most strategic feature is the ability to create different “employee classes.” This allows you to offer varied allowance amounts based on legitimate job-based criteria—like full-time vs. part-time status, salaried vs. hourly roles, or even geographic location—without violating nondiscrimination rules.

For example, a company with offices in both a high-cost urban area like San Francisco, CA, and a lower-cost rural area, could set a higher HRA allowance for employees based on the local cost of insurance. This ensures your benefits are fair and competitive, no matter where your team members live and work. This level of customization is a game-changer when comparing HRA vs. HSA options for a growing, multi-state business.

While a Health Reimbursement Arrangement (HRA) is an employer-funded allowance, a Health Savings Account (HSA) puts your employees in the driver’s seat. Think of it as a personal savings account for healthcare, owned and controlled entirely by the employee. This fundamental difference in ownership is one of the most important things to understand when comparing HRAs and HSAs.

The first rule of HSAs is straightforward: an employee can only open and contribute to one if they’re enrolled in a qualified High-Deductible Health Plan (HDHP). This pairing is intentional. The HDHP handles major medical events, while the HSA provides a tax-advantaged way for employees to save for and cover their out-of-pocket costs.

Unlike an HRA, the money in an HSA belongs to the employee for good. It’s their asset, rolling over every year and staying with them even if they change jobs, switch insurance plans, or retire. This portability turns a simple health benefit into a powerful financial tool.

The real power of the HSA comes from its famous “triple-tax advantage”—a benefit no other savings account can match. When explaining HSAs to your team, this is the feature you’ll want to highlight.

Here’s how it breaks down for your employees:

This unique structure means employees can pay for healthcare with dollars that have never been touched by taxes. It’s important to note that while this is true at the federal level, a few states (like California and New Jersey) tax HSA contributions and/or earnings at the state level. For a closer look at the mechanics, this guide on What Is A Health Savings Account? is a great resource.

HSA funding is incredibly flexible. Contributions can be made by the employee through payroll deductions, by the employer as a benefit, or even by a family member. Many employers choose to contribute to their employees’ HSAs to help them build a balance faster.

Each year, the IRS sets contribution limits. For 2024, the maximums are:

There’s also a key feature for older workers called the HSA catch-up contribution. Employees aged 55 and older can put in an extra $1,000 per year. This is a great way for those nearing retirement to give their savings an extra boost.

Keep in mind these limits are the total for both employer and employee contributions combined. If you want to dig deeper into the rules, you can learn more about what an HSA is and how funding works.

It’s easy to think of an HSA as just a way to pay for doctor visits and prescriptions, but that view misses its biggest strength. Because the funds roll over and can be invested, an HSA doubles as a long-term retirement savings account.

Once an employee turns 65, they can pull money out of their HSA for any reason without penalty. If the funds are used for non-medical expenses, they’re simply taxed as regular income—just like withdrawals from a 401(k) or traditional IRA.

This transforms the HSA into a secondary retirement fund. For employees who stay healthy and build a large balance, it provides a tax-free source for healthcare in retirement (one of life’s biggest expenses) and a flexible, penalty-free source of income for anything else.

When you put an HRA and an HSA side-by-side, the core differences come down to three things: who can join, who can put money in, and who owns that money in the end.

These aren’t just minor details—they get to the heart of what each account is designed to do. An HRA is a tool for employers to manage benefit costs, while an HSA is an asset for employees to build long-term financial security. Let’s break down what that means in practice.

The first major difference between an HRA and an HSA is who can even have one. An HSA has a single, non-negotiable rule: the employee must be enrolled in a qualified High-Deductible Health Plan (HDHP). No HDHP, no HSA. It’s that simple. This requirement ties the account directly to a specific health insurance strategy.

HRAs, on the other hand, are much more flexible. Eligibility depends entirely on which type of HRA an employer offers:

This flexibility allows employers to design benefits without being locked into an HDHP-only model—a huge advantage for businesses that want more options.

How money gets into the account is another area where HRAs and HSAs are worlds apart. HRAs are funded exclusively by the employer. Employees are not allowed to contribute their own money. It’s a reimbursement model where the employer sets an allowance, and that’s the total benefit available.

HSAs have a much more collaborative funding structure. Contributions can come from several places:

The real difference in philosophy is this: an HRA is a defined benefit allowance from the employer. An HSA is a defined contribution account that both the employer and employee can build together.

Contribution limits also look very different. The most flexible HRAs, like the ICHRA and GCHRA, have no federally mandated contribution limits, giving employers total control over their budget. The QSEHRA is the one exception, with annual caps set by the IRS.

HSAs, however, have strict annual contribution limits set by the IRS that apply to the combined total from all sources. For a complete guide on these rules, check out our breakdown of the maximum HSA contribution.

Perhaps the most important distinction when comparing HRAs and HSAs is ownership. It dictates what happens to the money and who truly benefits in the long run.

An HRA is owned by the employer. The funds are a company asset, not the employee’s personal cash. If an employee leaves or doesn’t use their full allowance, any leftover money is forfeited and returns to the business. This feature gives employers predictable costs and tight budget control.

In contrast, an HSA is owned entirely by the employee. It’s a personal savings account that is 100% portable. The funds stay with the employee for life, whether they change jobs, switch health plans, or retire. This makes the HSA a true long-term financial asset, not just a temporary health benefit.

| Factor | Health Reimbursement Arrangement (HRA) | Health Savings Account (HSA) |

|---|---|---|

| Who Owns the Account | The employer owns the account and all funds. | The employee owns the account as a personal asset. |

| What Happens at Separation | Unused funds are forfeited and return to the employer. | The account and its balance stay with the employee. |

| Long-Term Value | Provides immediate value for current medical costs. | Builds long-term value as a portable savings tool. |

Ultimately, the choice highlights a fundamental trade-off. HRAs give employers more control over their benefit spending. HSAs empower employees with a portable, appreciating asset that promotes financial wellness long after they’ve left the company. Your decision depends on whether your top priority is cost containment or helping your employees build wealth.

Knowing the difference between an HRA and an HSA is one thing. Applying that knowledge to your own business is another challenge entirely. The right choice always comes down to your company’s unique goals, budget, and workforce.

To help you connect the dots, we can walk through three common scenarios we see with our clients. Each one shows how a different health benefit can solve specific problems and support business growth. This is where the HRA vs. HSA discussion moves from theory into real-world decisions.

Let’s start with a small tech startup with 15 employees. Their top priorities are attracting talented developers with competitive benefits while keeping costs predictable and simple. A traditional group plan feels too expensive and rigid for their lean operation.

In this situation, an Individual Coverage HRA (ICHRA) or a Qualified Small Employer HRA (QSEHRA) is often the perfect fit. These HRAs let the startup set a fixed monthly allowance for each employee, which gets rid of the risk of sudden premium hikes. The company only pays for the funds that employees actually use for their health expenses.

For a lean business, the HRA model provides unparalleled budget control. It turns a volatile, unpredictable expense into a fixed, manageable line item, which is critical for early-stage companies where every dollar counts.

For this startup, an HSA isn’t the best option. It would require them to offer a group HDHP, bringing back the very premium costs and administrative headaches they want to avoid. The HRA gives them a much simpler path to offering great health benefits.

Now, picture a successful professional services firm—like an accounting or law practice—with 50 employees. Their main goal is to attract and keep top-tier professionals who expect benefits that support their long-term financial health. A simple reimbursement plan isn’t going to cut it; they need a benefit that also builds wealth.

Here, a High-Deductible Health Plan (HDHP) paired with a generously funded Health Savings Account (HSA) is the clear winner. The firm can offer a quality group HDHP and make a significant annual contribution to each employee’s HSA, like $1,500 for individuals and $3,000 for families.

This approach accomplishes a few key things:

For business leaders, investing in employee benefits is a strategic move that pays dividends. For this firm, the HSA directly aligns with its strategy of investing in its people for the long haul.

Finally, let’s look at a growing company with 100 employees spread across offices in Utah, Arizona, and Texas. They’re dealing with a common headache: healthcare costs and provider networks vary dramatically from one state to another. A single group plan that’s great in one city might be expensive and limiting in another.

The ideal solution here is an Individual Coverage HRA (ICHRA). The ICHRA’s most valuable feature is its ability to set different allowance amounts based on geographic location. This allows the company to use local market data to offer fair and competitive benefits to everyone, no matter where they live.

For instance, the company could offer:

This strategy creates benefit equity across the entire organization. It gives every employee the funds and freedom to buy a plan that actually works in their local market, solving the multi-state coverage puzzle that so many expanding businesses face. An HSA tied to a single group plan simply can’t provide this level of customization.

As you weigh your options between an HRA and an HSA, a few practical questions always come up. The details can feel complex, but getting them right is key to avoiding compliance headaches and employee confusion. We hear these questions all the time from business owners, so here are the clear answers you need.

Generally, the answer is no, but with important exceptions. IRS rules state that an individual cannot contribute to a Health Savings Account (HSA) if they are covered by any health plan that is not a High-Deductible Health Plan (HDHP). A standard, general-purpose Health Reimbursement Arrangement (HRA) is considered disqualifying “other coverage,” making an employee ineligible to contribute to an HSA.

However, an employee can contribute to an HSA while being covered by certain HSA-compatible HRAs:

Getting these distinctions right is critical. If you offer a general-purpose HRA to an employee who also has an HDHP, you could unintentionally disqualify them from making HSA contributions—a mistake that could cost them a valuable savings opportunity.

This is one of the biggest differences between an HRA and an HSA, and it has major financial implications for both you and your employees. The rules are straightforward.

With an HRA, the funds belong to the company. When an employee leaves—for any reason—any unused money in their HRA is forfeited and stays with the employer. This “use-it-or-lose-it” structure (unless rollovers are permitted) gives business owners total cost control.

With an HSA, the funds are the personal property of the employee. The account is 100% portable, which means the employee takes the entire balance with them when they go. That money is theirs to use for qualified medical expenses for life, no matter where they work next.

The core principle is ownership. HRA funds belong to the employer, providing budget certainty. HSA funds belong to the employee, offering a portable, long-term financial asset. This single difference often determines which plan best suits a company’s culture.

This distinction really frames the HRA as a benefit tied to current employment and the HSA as a lasting financial tool that empowers the individual.

The answer really depends on who you’re asking—the employer or the employee. Both plans are flexible, but in completely different ways.

For employers, the HRA offers much more flexibility in plan design. This is especially true if you use an Individual Coverage HRA (ICHRA). With an ICHRA, you can:

This makes the HRA a powerful option for employers who need a customized, budget-friendly benefits strategy that can grow and adapt with their workforce.

For employees, the HSA offers far greater financial flexibility and personal control. The power is truly in their hands. They get to:

This employee-centric flexibility makes the HSA a powerful financial wellness tool that goes beyond simple healthcare spending. Your choice really comes down to your primary goal: do you want to control the plan’s design (HRA), or do you want to empower your employees’ financial choices (HSA)?

Further Readings:

Unlock Affordable Health Benefits for Small Businesses in 2026

The Differences Between HSAs, FSAs, and HRAs

Unlock Growth with Outsourced HR Services Small Business

Navigating the complexities of HRA and HSA administration, compliance, and strategic design can be overwhelming. At Helpside, we simplify HR so you can focus on growth. We deliver expert guidance on benefits, payroll, and compliance, helping you build a benefits package that attracts top talent and fits your budget. Learn more about how Helpside can give you peace of mind at https://helpside.com.