Services

Payroll, benefits, HR, and risk management in one PEO solution.

You offer a 401(k) because you want to do right by your team and save for yourself. Then the year ends, your third-party administrator sends a compliance notice, and suddenly the plan that looked simple turns into refunds, corrections, and uncomfortable conversations with owners or key managers who thought they were on track.

That moment is where many small employers first learn what a safe harbor plan solves. It isn’t a niche retirement product. It’s a design choice that trades some flexibility for much more predictability. For a growing business, especially one with owners or leaders who want to maximize their own deferrals, that trade often makes sense.

The issue gets more complicated when your employees sit in more than one state. Federal safe harbor rules may be clear on paper, but payroll practices, compensation definitions, and retirement obligations can get messy once people work across Utah, Arizona, Idaho, Wyoming, or beyond. That’s where good plan design stops being theoretical and starts becoming operational.

A familiar small-business story goes like this. The owner defers aggressively. A few managers do too. Most employees contribute little or nothing. Then the plan fails testing, and the people who were most committed to saving are the ones who get money pushed back out of the plan.

That is exactly the frustration the safe harbor 401(k) plan is meant to reduce. Instead of hoping your plan passes its annual nondiscrimination tests, you build the plan so it gets an automatic pass on the main testing that causes trouble for small employers.

In practice, that means the employer commits to a required contribution formula and follows the related notice and plan rules. In return, the plan gets relief from the ADP and ACP tests that trip up so many traditional 401(k)s. For busy owners, the primary benefit isn’t abstract compliance. It’s certainty.

Practical rule: If your owners or highly paid leaders keep asking, “Will I get refunded again this year?” you’re already in the territory where a safe harbor plan deserves a serious look.

A safe harbor plan won’t solve every retirement-plan issue. It won’t erase payroll errors, fix weak employee communication, or remove state-by-state complexity for multi-state employers. But it does solve one of the most common reasons small business plans become unpredictable.

Traditional 401(k)s ask a small employer to keep a balancing scale level. On one side are highly compensated employees, often owners and senior leaders. On the other side are everyone else. The government wants to make sure the plan doesn’t mainly benefit the people at the top.

When participation and savings rates are uneven, that scale tips. That’s common in small businesses because leadership tends to save more consistently than the broader workforce. The result is annual testing pressure.

In 2020, a study of over 3,200 small business 401(k)s found that 26.47% of traditional plans failed the Actual Deferral Percentage (ADP) test, which means roughly one in four plans faced compliance failures that could trigger corrections and refunds to key employees, according to Employee Fiduciary’s small business 401(k) analysis.

The names sound technical, but the logic is simple.

For an owner, the consequences feel much more concrete than the acronyms suggest. The plan may require refunds to leadership, extra employer contributions, or corrective work with your TPA, payroll team, and recordkeeper.

A large company can absorb uneven participation more easily because it has a broader employee base. A smaller company usually can’t. If only a small group of employees contributes meaningfully, the owners’ behavior has an outsized effect on test results.

That creates a pattern many employers know too well:

The problem usually isn’t bad intent. It’s that a traditional plan assumes broad participation patterns that many small employers don’t actually have.

This is one reason retirement-plan decisions can’t be separated from the broader compliance landscape. A 401(k) doesn’t live in a vacuum. Payroll practices, eligibility tracking, onboarding, and employee communication all affect whether the plan works the way you expected.

Owners often try to solve testing issues informally. They remind employees to sign up. They wait and hope participation improves. They add a match without fully modeling how it will affect testing and budget.

Those moves can help, but they don’t create certainty. A traditional plan still leaves you exposed to annual results. If your main goal is to let leadership contribute confidently without year-end surprises, hoping for better participation usually isn’t a durable strategy.

A safe harbor plan is a 401(k) design that gives your plan an automatic pass on the ADP and ACP nondiscrimination tests, as long as you meet the required contribution and disclosure rules. That is the practical definition most business owners need.

The trade-off is straightforward. The employer agrees to contribute under an approved formula, and the plan gains predictable treatment under the federal testing rules that create so much friction in traditional plans.

According to John Hancock’s safe harbor 401(k) overview, a safe harbor 401(k) plan exempts employers from ADP/ACP testing by mandating specific employer contributions. That allows highly compensated employees, defined in 2025 as employees earning over $155,000, to maximize deferrals up to IRS limits without the same risk of forced refunds that affects many traditional small business plans.

A safe harbor plan works because the employer contribution isn’t optional in the same way a discretionary match is. The rules require a qualifying contribution approach, and those contributions generally must be vested immediately, depending on plan design.

That creates two big operational shifts:

Safe harbor plans matter most when your employee population isn’t likely to contribute in a pattern that supports a traditional 401(k). That often includes founder-led companies, family businesses, professional firms, and growing service businesses where leadership wants to save at a higher rate than the broader team.

A safe harbor plan is usually less about chasing a better retirement headline and more about solving a recurring operating problem.

Employers sometimes overestimate the benefit. A safe harbor plan removes the main ADP and ACP testing burden, but it doesn’t remove the need for careful administration.

You still need to get key items right:

That final point becomes more important as soon as your workforce spreads across jurisdictions. The safe harbor design may be federally sound, but the day-to-day mechanics still depend on accurate payroll and compensation treatment.

The right safe harbor plan usually comes down to one question. Do you want to reward employees who actively defer into the plan, or do you want a simpler employer contribution that reaches all eligible employees whether they contribute or not?

Most employers choose among three common approaches: basic match, enhanced match, and nonelective contribution. Each can work well. Each creates a different employee experience and a different budgeting pattern.

| Formula Type | Employer Contribution Requirement | Vesting Schedule | Best For |

|---|---|---|---|

| Basic Match | 100% on the first 3% of deferrals, plus 50% on the next 2% | Immediate vesting | Employers that want to encourage employee participation |

| Enhanced Match | More generous than the basic formula, such as 100% up to 4% | Immediate vesting | Employers that want a stronger recruiting or retention benefit |

| Nonelective Contribution | 3% to all eligible employees, whether they defer or not | Immediate vesting | Employers that want predictable coverage across the full eligible group |

The basic safe harbor match is familiar to many employers because it aligns the employer cost with employee action. If employees defer, they receive the match. If they don’t, the employer doesn’t match those missed deferrals.

The verified example is straightforward: under the basic formula, the employer contributes 100% on the first 3% deferred and 50% on the next 2%. On a $30,000 salary, an employee who defers 5% would receive a $1,050 employer contribution, as described in John Hancock’s explanation of safe harbor contribution formulas.

This formula usually fits employers that want to shape behavior. It tells employees, “If you save, we will too.” That can be useful when you want the retirement plan to drive participation rather than solely provide a baseline contribution.

An enhanced match must be at least as generous as the required safe harbor standard. The common appeal is competitive positioning. If you’re trying to recruit experienced employees, a richer match is easier to explain than a more technical plan feature.

The same John Hancock source gives an example of an enhanced formula at 100% up to 4%, which would be $1,200 on a $30,000 salary.

This option works well when leadership wants a stronger benefit story. The trade-off is obvious. A richer formula can improve the perceived value of the plan, but it also raises the expected employer commitment.

The 3% nonelective contribution goes to all eligible employees, whether they contribute or not. This is often the cleanest choice from an administration and fairness standpoint because it doesn’t depend on employee action.

That simplicity has real value. Employers with uneven participation, high turnover, or limited appetite for educating employees on match mechanics often prefer nonelective contributions because they remove guesswork.

It also changes the message. Instead of saying, “We match if you contribute,” you’re saying, “We fund a retirement contribution for you if you’re eligible.” Some owners like that because it feels more inclusive. Others dislike paying a contribution for employees who never choose to save on their own.

The formula should match your workforce behavior.

When employers choose poorly, it’s usually because they focus only on the headline formula and ignore payroll impact. Before finalizing the design, model the contribution against your compensation base, bonus practices, and eligibility rules. A good starting point is understanding how to calculate total employee compensation so the retirement formula is based on the same payroll reality your team administers.

Pick the formula you can fund consistently and explain clearly. The “best” safe harbor plan is usually the one your payroll team can run correctly and your employees can understand.

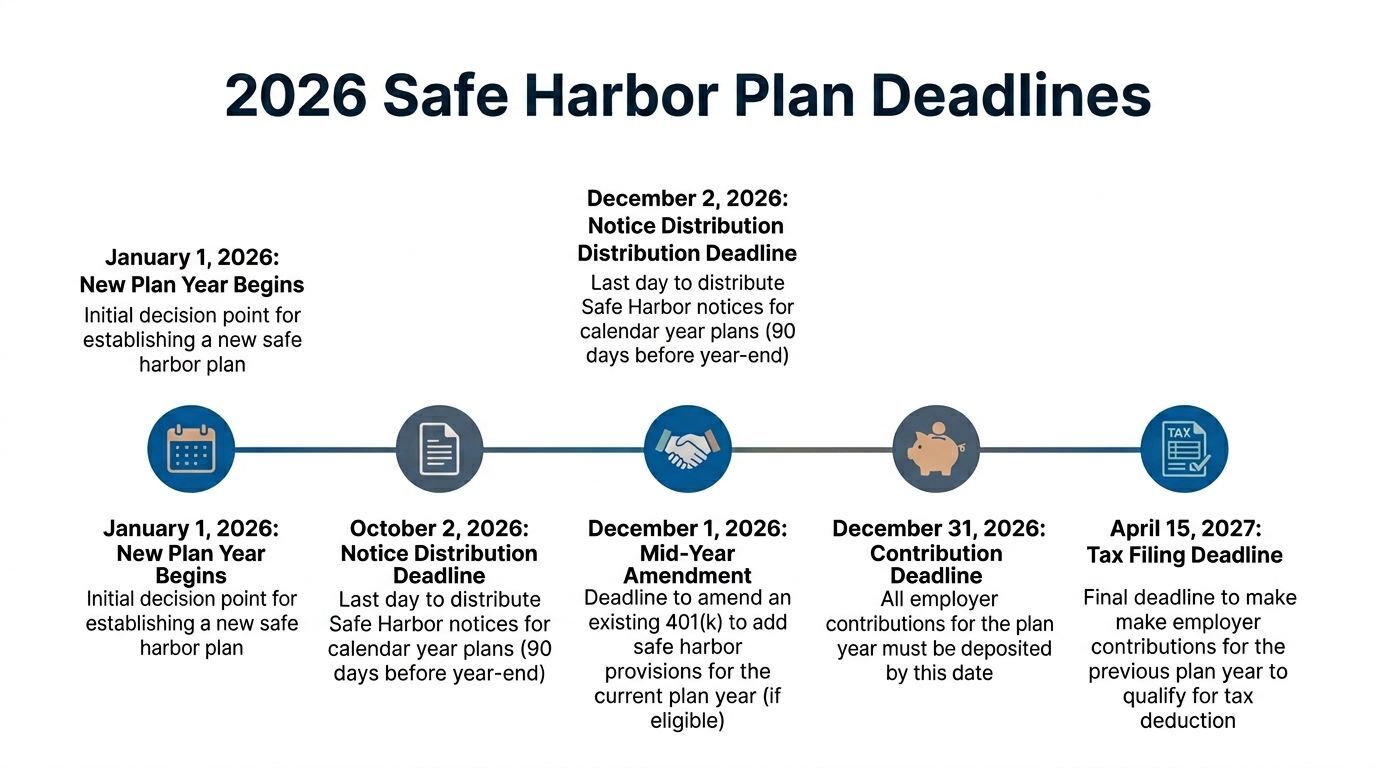

Safe harbor plans reward employers who make decisions early. They punish delay. If you’re considering a safe harbor plan for the 2026 plan year, timing matters almost as much as plan design.

Under the SECURE Act 2.0 framework, most new 401(k) plans established after December 29, 2022, must include automatic enrollment provisions by January 1, 2025, and for employers establishing a new safe harbor plan for the 2026 plan year, plan documents generally must be finalized by October 1, 2026 so there is enough time to provide the required 30-day advance notice, according to John Hancock’s discussion of safe harbor plan design deadlines.

A practical timeline for calendar-year employers looks like this:

The notice piece is where many employers slip. If your plan uses a match-based safe harbor design, the employee communication can’t be an afterthought. Employees need timely notice, and your payroll operation needs to be aligned with what that notice says.

Automatic enrollment isn’t just a plan feature anymore for many new plans. It’s now part of the legal framework. The SECURE Act 2.0 rules require default employee enrollment in a defined range and annual escalation under the conditions described in the verified guidance. That means safe harbor design now sits closer to payroll operations than it used to.

For small employers, this creates two practical questions:

Deadlines aren’t just legal markers. They’re operational deadlines for payroll, employee communication, and plan documents to say the same thing.

A safe harbor plan is one of those benefits where small documentation gaps can create outsized trouble. The notice has to match the plan. The plan has to match payroll. Payroll has to match actual deposits and elections.

That’s why retirement implementation should be part of your broader HR compliance for small business calendar, not a stand-alone benefits task. If the work is split across too many vendors, deadlines get missed in the seams.

A safe harbor plan is often a smart move. It is not always the cheapest move. Those are different questions, and owners do better when they keep them separate.

The strongest case for safe harbor is predictability. The strongest case against it is cost commitment. If your cash flow is uneven or your workforce changes quickly, that tension deserves a hard look before you adopt the plan.

The main upside is confidence for owners and other highly compensated employees. Safe harbor design lets those employees defer up to the applicable IRS limits without living under the annual threat of ADP and ACP refunds. The verified data allows citing the 2025 limits of $23,500 for elective deferrals and $70,000 for total additions from the earlier John Hancock safe harbor guidance.

The plan can also improve the employee value proposition. Immediate vesting on the required safe harbor contribution is easy to understand and generally appreciated by employees. In hiring conversations, that’s often much easier to communicate than a traditional plan that may or may not survive testing cleanly.

The downside is not subtle. You are committing to an employer contribution formula that has to be funded and administered correctly. That cost is no longer a year-end “maybe.”

There is also a flexibility trade-off:

| Decision factor | Safe harbor plan tends to fit when | Safe harbor plan tends to fit poorly when |

|---|---|---|

| Owner savings goals | Owners want confidence they can maximize deferrals | Owners aren’t prioritizing their own deferrals |

| Employee participation patterns | Broad participation is uneven or unpredictable | Participation is already strong and stable |

| Budget tolerance | The company can commit to a required employer contribution | Cash flow is too uncertain for a fixed formula |

| Admin capacity | The employer wants fewer year-end testing surprises | The employer values maximum contribution flexibility over predictability |

For companies weighing this against broader financial planning priorities, it can help to review how retirement costs fit within staffing, cash flow, and forecasting decisions, especially alongside outside CFO services consulting support.

A safe harbor plan works best when leadership is buying certainty on purpose. It works poorly when leadership adopts it reluctantly and then resents the contribution cost all year.

Safe harbor planning is often overlooked. Federal rules tell you how the safe harbor plan should be structured. They do not remove the complexity of paying employees correctly across multiple states.

That matters because safe harbor contributions must use a compliant definition of compensation under IRC Section 414(s). As the IRS explains in its guidance on compensation definition in safe harbor 401(k) plans, standard guidance often doesn’t address how that requirement interacts with multi-state payroll. For companies with employees across states such as Utah, Arizona, and Idaho, that creates a real compliance blind spot around state-specific pay rules and how those rules affect safe harbor contribution calculations.

The problem usually isn’t the plan document by itself. It’s the handoff between document language and payroll execution.

A few common friction points:

Multi-state employers should treat safe harbor administration as a coordination exercise between payroll, HR, and plan administration.

That means checking:

Federal safe harbor status solves one category of problem. Multi-state payroll discipline solves another.

A safe harbor plan can absolutely work well for a regional employer. It just needs tighter operational controls than most generic safe harbor articles ever mention.

A safe harbor plan becomes much easier to live with when the moving pieces sit under one roof. Most employers struggle not with the concept, but with the coordination. Payroll calculates contributions. A recordkeeper tracks deferrals. A TPA handles documents. HR fields employee questions. If those groups aren’t aligned, the plan feels fragile.

A PEO changes that operating model. Instead of asking your internal team to quarterback separate vendors, the PEO can help align payroll, HR administration, notices, onboarding, and compliance support around the same plan design. For a business owner, that means fewer handoffs and fewer opportunities for the plan document to say one thing while payroll does another.

A good PEO-supported process usually helps with:

For multi-state employers, that support matters even more. Expansion often breaks systems that seemed fine when everyone sat in one state. A PEO can help close the gap between federal retirement rules and the state-by-state realities of payroll and HR administration.

If you’re evaluating whether this type of model fits your business, it helps to understand what a professional employer organization takes on and where it can reduce risk.

The value isn’t that a PEO makes retirement plans glamorous. It doesn’t. The value is that it makes them more manageable. That matters when you’re trying to grow the business and don’t want every benefits decision to become a side project for finance, HR, and operations.

Ready to offer better benefits without the rising costs?

Call Helpside today for your Free 15-Minute Benefits Audit: 1-800-748-5102 and see how much time and money your business could save.

Further Readings:

A safe harbor plan can be a strong move for a growing company, especially when owners want predictable retirement outcomes and the workforce spans multiple states. If you want help evaluating whether that design fits your payroll, compliance, and benefits structure, talk with Helpside.